Index

Macro Update

by Dean Orrico, President & CEO and Robert Lauzon, CIO

Global markets ended the first half of the year near record highs, supported by a recent easing of Middle East geopolitical tensions and a surge in AI-related equities. Markets consolidated in June with the S&P 500 retracing 1.0% after gaining more than 16% over the prior two months, the index’s strongest quarter in six years, still returning 10.2% for the first half. The TSX Composite outperformed in June with a 0.5% gain and returned 11.2% during the first six months of 2026. The period also saw the successful listing of SpaceX, the largest IPO on record, paving the way for additional AI-related listings over the coming quarters.

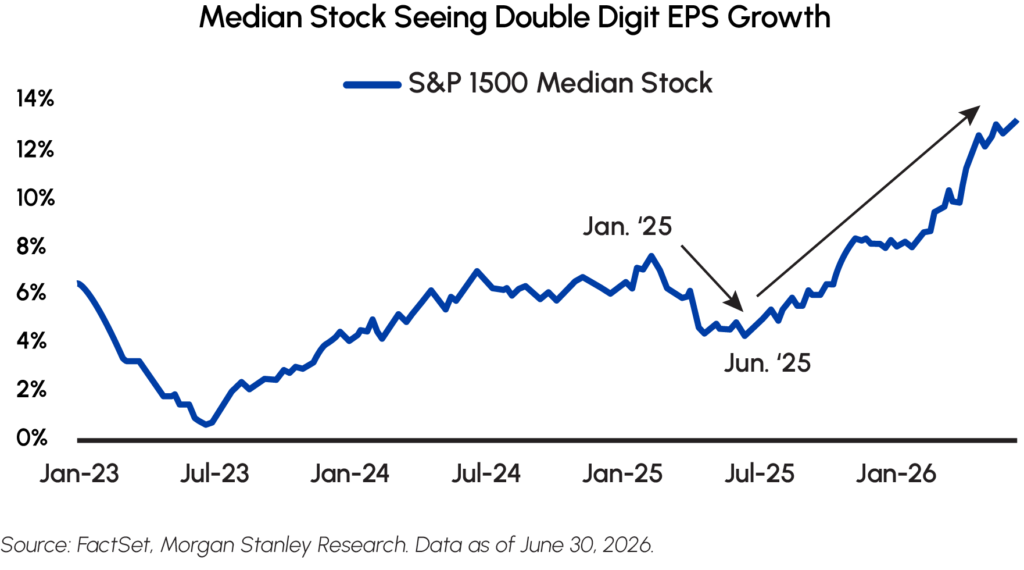

We view the June decline as a healthy consolidation and leadership rotation rather than the start of a broader market pullback. Specifically, we witnessed the rotation out of mega-cap tech and into other sectors pushing the S&P 500 equal-weight index to record highs even as the cap-weighted index declined. We think this reflects an earnings recovery the market hasn’t fully priced in. Earnings growth for the median S&P 1500 company has hit double digits (as seen in the graph below), the strongest pace in years, as reviving revenue growth flows through lean cost bases and produces outsized operating leverage. Investors are growing more concerned about heavy capex spending and its ultimate return on investment from the Mag-7. Healthcare was the second best-performing S&P 500 sector with a 6.6% return in June alone. We are especially constructive on biotech, where our Middlefield Healthcare strategies have meaningful exposure via a proprietary model with our partners at SSR Health.

Canada’s federal government has been moving aggressively on major infrastructure initiatives through the Building Canada Act and its Major Projects Office (MPO), which fast-tracks federal approvals for projects deemed in the “national interest.” Prime Minister Carney’s government is attracting foreign investors and capital as they advance initiatives spanning LNG, nuclear, critical minerals, and transportation. On the pipeline front, Canada and Alberta have agreed on a west coast pipeline proposal alongside the Pathways carbon capture initiative. Most TSX sectors advanced in June, led by Financials, while Materials was the most volatile sector as gold stocks reversed sharply late in the month as geopolitical risk eased and rate-cut expectations diminished. Real Estate outperformed the broader market while our REIT strategies continued to beat the benchmark. Four of the top five contributors to our June outperformance came from high-conviction, out-of-benchmark positions, underscoring our long-term track record of adding value through active management. It’s clear that market broadening is also occurring within the TSX. More specifically, while outperformance in 2025 was led by the rally in gold, 2026 is being driven by financials and energy, two sectors where Canada is a global leader and foreign investors are taking note.

New Fed Chair Kevin Warsh held rates steady at his inaugural FOMC meeting while delivering a hawkish surprise, explicitly abandoning forward guidance and introducing a new layer of policy uncertainty. The market has moved from pricing in multiple 2026 rate cuts earlier in the year to now pricing in a hike, driving a material rise in the U.S. Dollar Index. At the Sintra conference, Warsh strictly defined price stability as returning inflation to its 2.0% target, addressing a five-year overshoot, and by declining to offer forward guidance, he signaled that financial markets and bond yields, rather than Fed promises, will dictate the policy path ahead.

Fixed Income

Middlefield Fund Tickers & Codes: MSBP / MID 435

by Gordon McKay, Senior Portfolio Manager

June’s positive returns were driven by continued income harvesting alongside small price gains as Canadian interest rates moved slightly lower and credit spreads widened by a couple basis points. Smaller concessions resulted in the team being much more selective investing in new issues during June. For the second straight month, MSBP participated in a inaugural Canadian Maple bond issued by a hyperscaler, this time Amazon. However, we declined to participate in SpaceX’s first bond deal, which ended the month 10-20bps wider. CES Energy Solutions issued new bonds to retire the tranche previously held by MSBP. The Fund rolled its investment into the new bonds of this quality, high yield issuer. MSBP also invested in a mortgage-backed security with the underlying retail real estate assets offering an attractive return profile and AAA rating. The new investment pushed duration and currency adjusted yield to maturity modestly higher to 1.2 years and 3.99%, respectively.

MSBP continues to focus on enhancing returns by maximizing exposure to embedded upside options in corporate bonds. Tilting the portfolio towards bonds trading below their call price allows for positive surprises. Outfront Media called it’s 5% note due in 2027 14 months early. The Fund realized a 5.47% annualized return on its Outfront position over the 3-month holding period – outpacing the yield to maturity of 5.08% of the bond. This is a prime example of embedded options enhancing MSBP’s returns without adding risk.

Real Estate

Middlefield Fund Tickers & Codes: MREL / MID 600 / RS / RS.PR.A

by Dean Orrico, President & CEO

The S&P/TSX Capped REIT Index delivered broadly positive returns in June, with most constituents posting gains in CAD terms, lifting its YTD total return to an impressive 13.6%. Notably, Canadian REITs have outperformed the TSX Composite (+11% YTD). The Canada 10-year government bond yield declined by 14.9 bps from a high of 3.529% on Jun 8 and provided a constructive tailwind for rate-sensitive REIT valuations. Our Real Estate funds continued to perform well with total returns of 4.5% in June and approximately 14.5% YTD. Our high conviction, active management investment style, with approximately 30% of portfolio assets outside of Canada, remains a major contributor to outperformance. Welltower and Ventas, two of our core U.S. healthcare real estate companies, were up approximately 11% and 6% respectively during the month, driven primarily by a powerful sector-wide tailwind on aging demographics and constrained new supply, driving occupancy and margin expansion across the industry. Welltower also raised their dividend by 15% to $0.85/share, signaling confidence in cash flow growth. Similarly, Ventas reaffirmed FY2026 FFO/share guidance in line with consensus.

Stock selection within our underweight Industrial REITs was additive to performance. Granite REIT and Dream Industrial have significantly inflected higher since their lows earlier in the year. Segro PLC, another long-term industrial property holding with a dominant position in the UK and Europe, was up approximately 20% in June after a takeover offer from Prologis REIT (another high-quality Industrial REIT we’ve owned for several years). We met recently met with Segro’s management team and were pleased with the takeout offer, given the underlying fundamentals were not being appropriately rewarded by the public markets.

US Homebuilders also caught a bid in June on better industry fundamentals including existing home sales beat, pending home sales surge and Congress passing new housing affordability legislation. We own PulteGroup and Toll Brothers which were up approximately 17% and 19%, respectively. Toll Brothers outperformed on sell-side upgrade and price target raises. Luxury buyers have also proven more resilient with demand more sensitive to employment and equity markets than mortgage rates.

We continued to see consolidation in the sector with Blackstone potentially acquiring specific H&R REIT’s assets, causing H&R to surge more than 8% on June 12. In addition, the Ontario Superior Court approved the C$9.4B acquisition by Choice Properties and KingSett Capital of First Capital REIT, with closing expected in Q4 2026. These M&A activities are the latest example of dislocated public market pricing, sparking stronger interest in names from deep-pocketed institutional investors where heavily discounted valuations persist.

We are encouraged to see the market broadening out and believe Real Estate will continue to provide investors with a decent return given improving fundamentals and lower volatility.

Healthcare

Middlefield Fund Tickers & Codes: MHCD / MID 325 / SIH.UN

by Dean Orrico, President & CEO

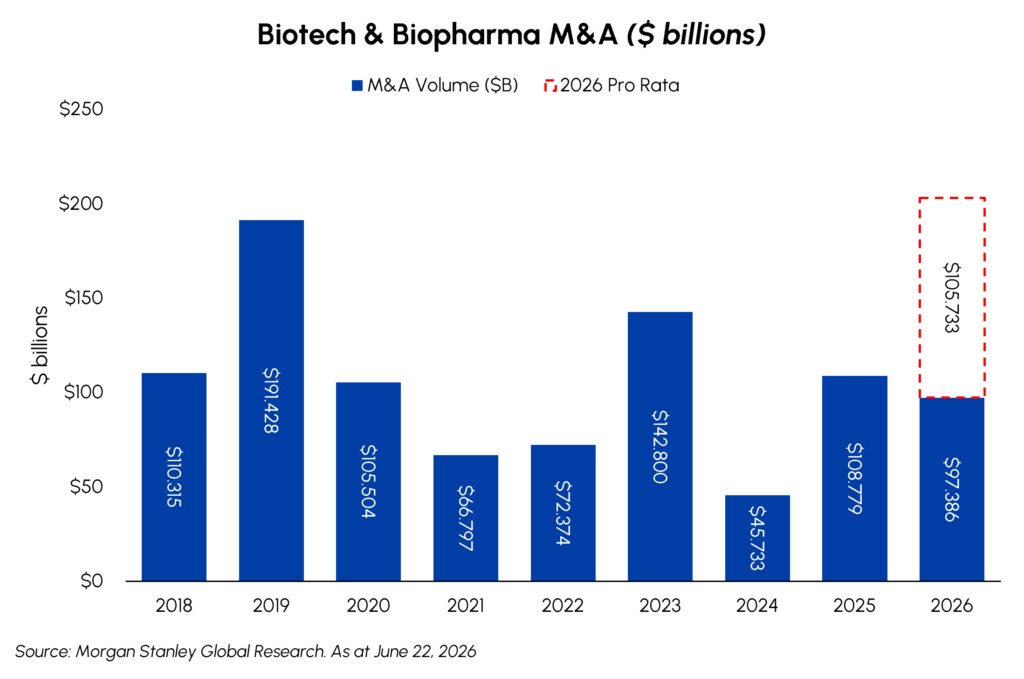

Healthcare had a terrific month, with the broad sector up 6.4% and each sub-sector participating in the rally. The last week of June was the sector’s 2nd best performing week in the last 10 years (excluding COVID). Biotech and pharma led the charge, each gaining ~10% on the month. Biotech has been the real standout and is now the top-performing sub-industry within US healthcare year-to-date, up 30%, after decisively breaking out from its multi-year period of underperformance. The rally has been powered by investor rotation back into the group, a wave of dealmaking (industry M&A is tracking for its best year ever), and positive clinical trial and regulatory news.

A standout example of the M&A environment was AbbVie’s ~$11 billion acquisition of Apogee Therapeutics, a clinical-stage biotech focused on inflammatory diseases, in a deal that proved a clear win for both sides. Apogee holders received nearly a 50% premium, while AbbVie gained a pipeline that extends its immunology franchise well beyond current blockbusters Skyrizi and Rinvoq. Other notable deals include GSK/Nuvalent ($10.6 billion) and smaller biotech consolidation such as Incyte/Vega Therapeutics. Biopharma has also benefited from a steady stream of positive clinical and regulatory news, including from two of our core holdings. Merck secured a series of FDA approvals in June that both extended its flagship cancer drug Keytruda into new tumor types. Meanwhile, Eli Lilly posted strong late-stage data for orforglipron, its weight-loss pill that outperformed Novo Nordisk’s and offers a convenient alternative to injectables.

We remain constructive on Life Science Tools despite the sub-sector slightly lagging the rest of healthcare this month. The industry backdrop has strengthened, driven by year-over-year gains in pharmaceutical spending, new drug approvals, clinical trial starts, licensing activity, and biotech funding. The much-discussed AI overhang presents an opportunity rather than a threat: while AI may streamline the earliest stage of drug discovery, it should drive far more of the downstream laboratory work for these companies. This includes testing, validation, and quality control that follow as more drug candidates advance through the pipeline.

Infrastructure

Middlefield Fund Tickers & Codes: MINF / MID 265 / MID 510 / ENS / IS / IS.PR.A / MID 800

June brought a landmark development for Alberta’s data centre buildout, as Pembina Pipeline announced positive FID on the Greenlight Electricity Centre, a 932 MW natural gas-fired power project developed alongside Kineticor. The $4.6 billion project is underpinned by a long-term supply agreement with a major hyperscale customer (widely believed to be Meta) and is expected online in the second half of 2030. Beyond its direct economics, the Greenlight deal marks the first major data centre power project to reach FID in Alberta, effectively validating the province’s emerging thesis as a North American AI infrastructure hub and opening the door to further announcements.

This has direct read-through for two of our core infrastructure holdings, TransAlta (TA) and Capital Power (CPX). Both companies stand to benefit from tightening Alberta power pricing and rising volumes as data centre load materializes, with the potential to monetize underutilized generation capacity ahead of new builds coming online. Capital Power is expected to serve as a power supplier to the Greenlight project under an existing MOU. TA and CPX continue to anchor our Infrastructure and Diversified funds, giving us exposure to Alberta’s data centre buildout. Both have delivered solid year-to-date returns, with Capital Power up 22% and TransAlta up 10%.

On the pipeline front, the federal and Alberta governments unveiled a proposal for a 1 million barrel-per-day oil pipeline to the West Coast, following a revised southern route along the existing Trans Mountain corridor. The consortium includes Trans Mountain Corporation, the Alberta Petroleum Marketing Commission, and Pembina Pipeline, which holds an initial 10% stake with an option to increase to 20% at commercial operation. While still in early stages, given that FID is not expected until 2028, the project represents a meaningful step toward diversifying Canadian crude exports and will benefit the broader Canadian midstream complex over time as egress capacity expands.

Looking ahead, our team will be attending an industry conference in Calgary this month, meeting directly with management teams across several of our core holdings including Enbridge and Topaz Energy. Topaz continues to benefit from rising production volumes through its take-or-pay royalty and infrastructure model, supporting a stable and attractive 4% dividend yield. We look forward to sharing updates from these conversations in future commentary.

Technology & Communications

Middlefield Fund Tickers & Codes: MINN / SIH.UN / MID 925 / MDIV

by Shane Obata, Portfolio Manager

June served as a reminder that even strong secular themes need to pause. Technology stocks, particularly AI-linked semiconductors, went through a sharp but healthy pullback as investors reassessed positioning, valuation and the scale of AI capital spending. We do not view this as a sign that the AI buildout is weakening. Rather, we see it as a normal reset inside a powerful earnings cycle, and one that reinforces the importance of being selective.

Our north star remains earnings growth. On that measure, Technology continues to stand out. Goldman Sachs estimates that AI infrastructure companies could account for nearly 60% of total S&P 500 earnings growth in the second quarter, with Nvidia and Micron alone contributing more than 40%. That is an extraordinary statistic, and it helps explain why we remain focused on the companies enabling the physical AI buildout rather than treating recent volatility as a reason to reduce exposure.

The key distinction is that AI leadership is becoming more refined. The market is no longer rewarding every AI-related company equally. We continue to favor areas where demand is visible, supply is constrained and pricing power is improving. This includes semiconductor equipment, memory, advanced substrates and other bottlenecks. At the same time, we are more selective in areas where investor expectations have moved faster than fundamentals, including parts of the optical supply chain where adoption timelines can be uneven.

Importantly, we have maintained an underweight position in the Magnificent Seven throughout 2026. That has given us a valuable source of funding to own companies that benefit from AI capital spending without necessarily bearing the same return-on-investment scrutiny as the largest capital spenders. Investors have become more sensitive due to the sheer size of hyperscaler investment plans

We have used that opportunity to build exposure to AI bottlenecks, particularly in Asia, where many of the most important “picks and shovels” of the buildout are located. This has created a double benefit: the market has punished some of the largest AI capital spenders while rewarding the suppliers providing the memory, equipment, substrates and infrastructure required to make AI scale. We do not expect that distinction to disappear quickly. The AI trade is maturing, but the earnings opportunity remains very much alive.

Resources

Middlefield Fund Tickers & Codes: MID 800 / MID 161 / MID 265 / MRF FT LP / Discovery FT LP

by Dennis da Silva, Senior Portfolio Manager

Gold and gold equities significantly underperformed broad North American markets in June, for the fourth consecutive month, with gold down 11.7% versus the 13.2% decline of the S&P/TSX Gold Index. The selloff in gold miners has driven equity valuations to multi-year lows. Despite the decline in bullion, gold miners are well positioned: (1) cost discipline has been much better vs previous cycles with near record margins better positioned to absorb lower gold prices; (2) balance sheets remain solid with mostly net cash positions; (3) spot free cash flow continues to provide scope for supportive/accretive buybacks; (4) management teams have remained disciplined on capital allocation, with lower valuations & strong balance sheets providing attractive M&A opportunities in a downcycle. While near-term gold catalysts remain muted, we view this as consolidation rather than a structural break in the gold investment thesis. For patient investors, this may well be remembered not as the end of the gold cycle, but as one of its most compelling entry points.

Global energy markets shifted from a Middle East-driven supply shock at the start of June to a fragile calm by month’s end. This transition left oil and gas markets to grapple with the divergence between falling prices and a genuinely stabilized physical market. While the physical oil market surged during the early stages of the Iran war, it is expected to stabilize as pent-up volumes from the Strait of Hormuz—previously bottlenecked by curtailed production and logistical headwinds—are finally released. Furthermore, sentiment should be bolstered by inventory restocking, fueled by recent announcements of elevated national reserve targets. U.S. natural gas markets showed notable stability despite the geopolitical backdrop, something we have previously highlighted given relative supply security in North American markets, even as demand grows from planned LNG capacity additions through the end of the year. El Niño may potentially intensify weather events that vary globally and affect key regions differently, in a year when we are already seeing extreme heat unfold in Europe. The Middle East conflict has pushed out global gas oversupply by at least 1 to 2 years, and international gas consumers may now look to diversify their supply sources – supporting more growth for Canadian producers. Current low inventory in Europe and Asia underpin the bull case, augmented by lingering geopolitical risk. We expect global gas prices will strengthen through summer as Europe continues to refill inventories.

Although Canadian oil & gas equities have materially outperformed year-to-date, we continue to see upside in select stocks. In our view, stock returns were relatively tepid during the recent oil price surge, leaving valuation multiples compressed and free cashflow yields elevated. Canadian natural gas stocks have lagged due to depressed AECO pricing, driven in part by mild winter weather in western North America, resulting in elevated regional storage. However, the outlook is improving with demand tailwinds from increasing LNG exports and data centre buildout with near term catalysts being the final approvals of LNG Canada Phase 2 and Ksi Lisims potentially in the latter half of the year. The S&P/TSX Capped Energy Index was down 7.9% in June, driven by the ~ 20% decline in the WTI price.

Exchange Traded Funds (ETFs)

Mutual Funds (FE | F)

TSX-Listed Closed-End Funds

| Fund | Ticker | Strategy |

|---|---|---|

| MINT Income Fund | MID.UN | Equity Income |

| Sustainable Innovation & Health Dividend Fund | SIH.UN | Innovation & Healthcare |

TSX-Listed Split Share Corps. (Class A | Preferred)

| Fund | Ticker | Strategy |

|---|---|---|

| E-Split Corp. | ENS | ENS.PR.A | Energy Infrastructure |

| Real Estate Split Corp. | RS | RS.PR.A | Real Estate |

| Infrastructure Dividend Split Corp. | IS | IS.PR.A | Infrastructure |

LSE-Listed Fund

| Fund | Ticker | Strategy |

|---|---|---|

| Middlefield Canadian Enhanced Income UCITS ETF | LSE: MCTC | LSE: MCTP | Canadian Equity Income |

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments, including ETFs. Please read the prospectus before investing. You will usually pay brokerage fees to your dealer if you purchase or sell units/shares of investment funds on the Toronto Stock Exchange or other alternative Canadian trading system (an “Exchange”). If the units/shares are purchased or sold on an Exchange, investors may pay more than the current net asset value when buying and may receive less than the current net asset value when selling them. There are ongoing fees and expenses associated with owning units or shares of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in these documents. Mutual funds and investment funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain statements in this disclosure are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may”, “will”, “should”, “could”, “expect”, “anticipate”, “intend”, “plan”, “believe”, or “estimate”, or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what Middlefield Funds and the portfolio manager believe to be reasonable assumptions, neither Middlefield Funds nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

This material has been prepared for informational purposes only without regard to any particular user’s investment objectives or financial situation. This communication constitutes neither a recommendation to enter into a particular transaction nor a representation that any product described herein is suitable or appropriate for you. Investment decisions should be made with guidance from a qualified professional. The opinions contained in this report are solely those of Middlefield Limited (“ML”) and are subject to change without notice. ML makes every effort to ensure that the information has been derived from sources believed to reliable, but we cannot represent that they are complete or accurate. However, ML assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. ML is under no obligation to update the information contained herein. This document is not to be construed as a solicitation, recommendation or offer to buy or sell any security, financial product or instrument.