Index

Macro Update

by Dean Orrico, President & CEO and Robert Lauzon, CIO

Global equity markets rebounded sharply in April, with both the S&P 500 (+10.5%) and TSX Composite Index (+3.8%) recovering from March lows and hovering near all-time highs. The rally was triggered by early signs of de-escalation in the Iran conflict, easing concerns around prolonged energy supply disruptions and their knock-on effects on global growth. With peak pessimism already priced in and light positioning, markets responded swiftly to an exceptional Q1 earnings season. While valuations have reset higher and the near-term risk/reward setup appears more balanced, investor focus has decisively shifted back toward positive forward earning revisions.

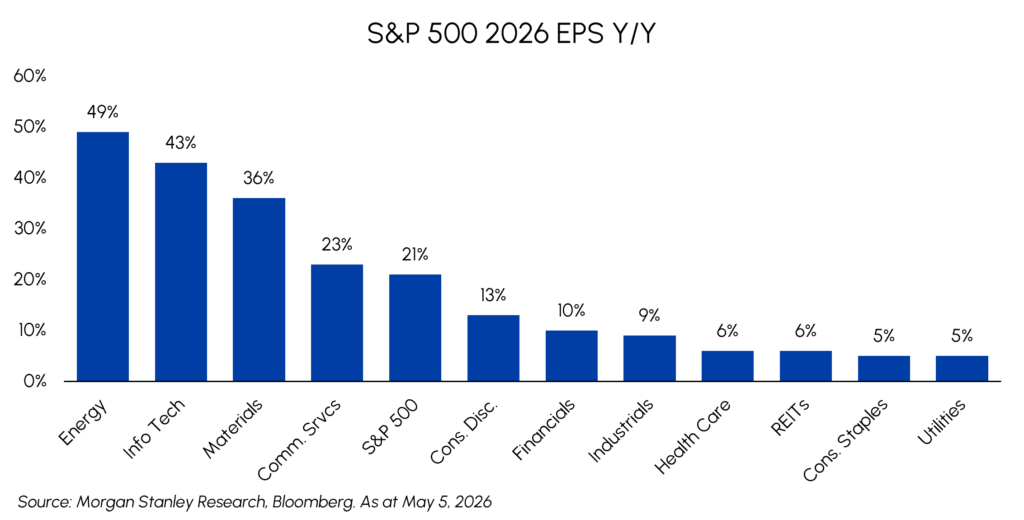

As mentioned, Q1 earnings season has been a key driver of the rebound with S&P500 earnings growth tracking closer to 28% Y/Y well above initial expectations of ~14%, with the median company posting 16% growth and 6% earnings beat (the strongest in 4 years). The breadth and magnitude of these beats have reinforced confidence in corporate resilience despite recent macro volatility. Technology and Communication Services led the rebound, driven by strong results from semiconductors and hyperscalers, reasserting leadership after earlier volatility as investors refocus on growth, innovation, and secular demand trends. As depicted below, full year 2026 EPS growth forecasts for Energy and Technology are significantly above market average, benefiting our sector-focused strategies (MAEC/ MINN) which emphasize high-quality companies delivering strong earnings beats and trading at attractive valuations. The combination of improving fundamentals and supportive earnings revisions reinforces our conviction in these sectors as durable drivers of performance.

On the policy front, both the Federal Reserve and the Bank of Canada held policy rates steady in April, signaling a more patient stance amid evolving macro conditions. While March inflation readings came in hotter, partly reflecting the lagged impact of higher energy prices tied to the Iran conflict, central banks remain focused on balancing inflation risks with growth stability. Market expectations have shifted meaningfully, with U.S. rate cuts now largely pushed out, and some probability assigned to a rate hike, while Canadian markets are pricing in potential easing later in 2026. Historically, periods where central banks are on hold alongside above-trend earnings growth have supported strong equity returns, reinforcing the current market backdrop.

Fixed Income

Middlefield Fund Tickers & Codes: MSBP / MID 435

by Gordon McKay, Senior Portfolio Manager

April’s positive returns were driven by disciplined income harvesting, underscoring the Fund’s ability to generate carry in challenging markets. Gains from tightening credit spreads were largely offset by higher interest rates that pressured government bond holdings. As rates backed up, the currency adjusted yield to maturity increased 12 bps to 3.74%, with duration essentially unchanged at 1.23 years.

The Fund continues to broaden its exposure as opportunities arise. During a heavy issuance month for Canadian corporates, elevated volatility around the war created attractive new issue concessions. The Fund selectively participated in several deals, capturing favourable entry points; all but one of these new holdings has already benefited from spread tightening.

With interest rates volatile and credit spreads tight, the Fund remains focused on maximizing income while managing risk. We continue to seek opportunities to diversify, reduce volatility, and offset tail risks while enhancing yield through new issues that are offering favorable terms. The Fund is well positioned to deploy selectively into further yield backup or spread widening, with capacity to add both credit and duration within established risk tolerances.

Real Estate

Middlefield Fund Tickers & Codes: MREL / MID 600 / RS / RS.PR.A

by Dean Orrico, President & CEO

Real estate participated meaningfully in the April equity rebound, with Middlefield’s real estate funds delivering solid results as MREL and MID601 generated returns of +5.5% and +5.1% respectively, reflecting both the broader sector recovery and the impact of company-specific catalysts within the portfolio.

The second quarter started on a high note for our real estate funds with the announced acquisition of First Capital REIT, one of our longest-standing core holdings, by Choice Properties REIT and KingSett Capital in a $9.4 billion transaction. The deal is proposed to be completed at an 8% premium to reported NAV, a particularly noteworthy outcome versus the more recent Canadian REIT takeovers completed at a discount to NAV. This is the third Canadian REIT acquisition in the past twelve months, and reinforces a view we have held for some time — our core REIT holdings are trading at a meaningful discount to intrinsic value, and where public markets are slow to recognize that gap, well-capitalized private buyers will step in.

Within seniors housing, structurally constrained supply and accelerating demand continue to drive increased occupancy and operating leverage across our core holdings in Welltower, Extendicare, Sienna, and Chartwell, all of which are experiencing significant NOI growth as the broader “silver economy” accelerates. Extendicare in particular stands out, with 43.7% returns year-to-date, driven by a 15% increase in average daily volume and a transformational home care acquisition that is tracking well ahead of initial underwriting, positioning the company for AFFO growth that ranks at the top of its peer group through 2027. We’re very constructive on the AI infrastructure build-out through Equinix, a leading global data center REIT whose interconnection platform sits at the center of growing cloud and AI workloads. Equinix has generated a return exceeding 40% year-to-date and reflects our conviction that physical digital infrastructure remains one of the most durable secular growth themes in real estate.

An out-of-favour industry where we continue to have high conviction is real estate services, where Colliers and FirstService offer durable compounding potential that the market is currently underappreciating. Colliers has faced recent selling pressure on fears that AI could disrupt brokerage and advisory work, a concern we view as overstated given the relationship-driven and highly complex nature of large capital markets mandates. We see the current weakness as an attractive entry point with the company projecting mid-to-high teen capital markets revenue growth in 2026 and a path back to prior peak revenues by end of 2027. FirstService is delivering steady growth across its residential property management and brands segments. While near-term softness in discretionary categories such as home improvement and roofing has weighed on sentiment, the company’s defensive recurring revenue streams, consistent contract wins, and strong execution underpin our confidence in a return to normalized growth. Both businesses are led by management teams with exceptional long-term track records of disciplined capital allocation and value creation, significantly supporting our high conviction in both names.

Healthcare

Middlefield Fund Tickers & Codes: MHCD / MID 325 / SIH.UN

by Dean Orrico, President & CEO

Even though defensive sectors like healthcare lagged in April, Managed Care emerged as a standout area of outperformance because of two meaningful catalysts. Firstly, the final 2027 Medicare Advantage benchmark rate increase of 2.48% came in above investor expectations, alleviating a significant overhang and improving visibility around 2027 margin recovery. This was reinforced by Q1 earnings which cleared a very low bar due to medical cost trends largely in line with pricing assumptions and early signs of member usage of services aligning with expectations. We maintain exposure through UnitedHealth and Humana, both of which stand to benefit as stabilizing cost trends translate into earnings visibility in the latter half of 2026.

Artificial intelligence is rapidly becoming a structural force across the entire drug development cycle, impacting everything from molecule design and target identification to clinical development and diagnostics. We believe this does not reduce demand for physical laboratory infrastructure, as more candidates advancing through the pipeline translates directly into greater utilization of instruments, consumables, and research services that power the innovation engine. With Life Science Tools & Services trading near 10-year trough valuations, we view the long-term, AI-driven demand inflection as an underappreciated catalyst. As a result, we are overweight the segment through positions in Thermo Fisher Scientific and Danaher.

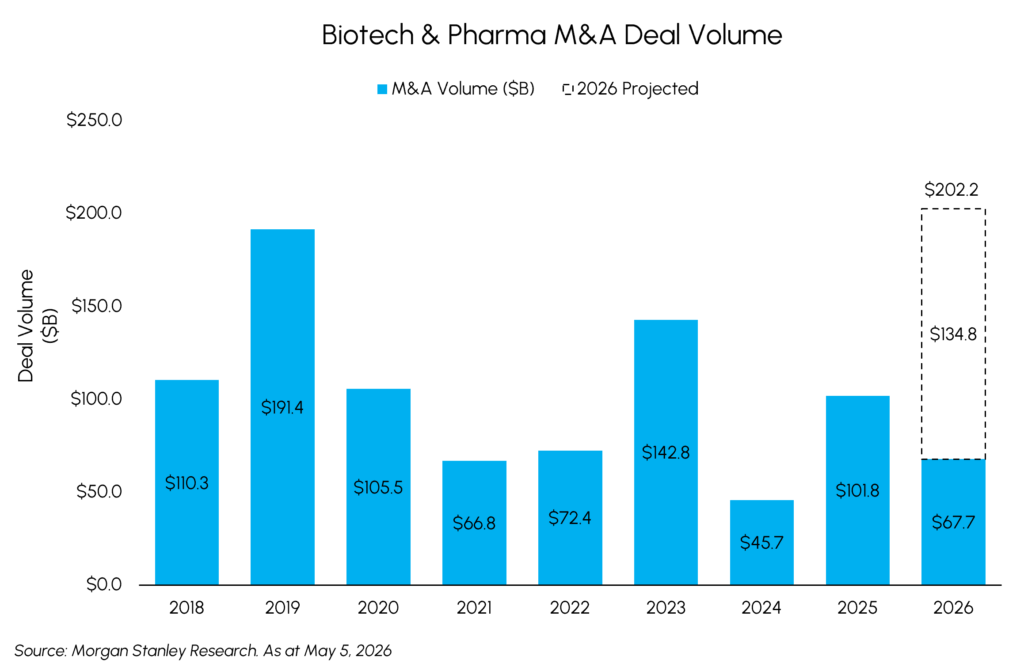

Eli Lilly is demonstrating why it remains one of our highest-conviction holdings, with the company capitalizing on the commercial momentum of its GLP-1 franchise to aggressively pursue growth through acquisition. Lilly is actively deploying capital to backfill longer-dated pipeline gaps, a disciplined approach to sustaining growth well beyond the current product cycle. This acquisition activity is emblematic of a broader trend as biotech and biopharma M&A is tracking toward its highest deal value in eight years as shown below. This reflects large-cap pharma’s growing urgency to replenish pipelines ahead of a significant patent cliff. With respect to MedTech, Q1 earnings confirmed that procedure volumes remain a source of inelastic demand, proving resilient across the board and reinforcing our view that near-term macro concerns have been disconnected from underlying fundamentals. Intuitive Surgical was a notable standout, delivering solid results that reinforced our conviction in robotic-assisted surgery as one of the most durable multi-year growth themes in the sector.

Infrastructure

Middlefield Fund Tickers & Codes: MINF / MID 265 / MID 510 / ENS / IS / IS.PR.A

Infrastructure equities remained positive in April, though performance moderated after a strong start to the year. Canadian Energy Infrastructure continued to benefit from improving sentiment around large-scale project development and a solid start to the earnings season. Enbridge received approval for its $4B natural gas pipeline in British Columbia, expected to enter service in late 2028, and add ~300 million cubic feet per day of additional capacity. Ongoing progress on Ksi Lisims and LNG Canada Phase 2 further reinforces Canada’s position as a critical global energy supplier. Shell’s recent $22B acquisition of ARC Resources, alongside reported interest from other global players highlights growing international appetite for long-life, scalable Canadian natural gas assets. Together, these developments are driving a more constructive outlook for infrastructure investment, with governments and private capital increasingly aligned on advancing energy security and export capacity.

The Presidential permit for the Bridger Pipeline expansion marks a meaningful step forward for Canadian crude export capacity. The project envisions a 36-inch, 450,000 b/d pipeline running 645 miles from the Canadian border through Montana and Wyoming to Guernsey — a key Rockies crude hub — largely following existing rights-of-way, which keeps costs and permitting risk lower than a greenfield route. On the Canadian side, South Bow (SOBO) is evaluating its complementary Keystone Prairie Connector project following shipper engagement. We expect strong commercial appetite for the additional egress supported by a recent Reuters article suggesting SOBO is close to securing the minimum commitments from oil companies; directionally signaling broader confidence the project proceeds. This builds further on other Canadian oil export initiatives already underway, including Enbridge’s Mainline Optimization (Phase 1 adding ~150,000 b/d by next year, Phase 2 up to 250,000 b/d by 2028) and TMX’s proposed capacity increases via drag-reducing agents. Taken together, these developments represent a materially improved egress outlook for Canadian producers — a constructive backdrop for the sector heading into the back half of the year.

AltaGas, a core infrastructure dividend grower, delivered better than expected Q1 results, highlighting its leverage to rising global demand for Canadian Liquid Petroleum Gas (LPG). The company continues to benefit from elevated pricing and volumes, particularly into Asian markets, where geopolitical tensions have reinforced the need for reliable supply. AltaGas’ export platform, including RIPET (propane export terminal) and the ongoing REEF expansion, is driving increased throughput and capacity, positioning the company to capture incremental demand as volumes ramp.

Beyond energy, other infrastructure segments have also contributed positively to fund performance. Transportation equities such as Mullen Group and Getlink have performed well year-to-date supported by resilient economic activity, reshoring trends, and increased demand for freight and logistics services. In Utilities, leading platforms including NextEra Energy and RWE continue to benefit from significant capital investment cycles aimed at modernizing power grids and expanding generation capacity. These investments are critical to meeting rising electricity demand from data centers, industrial activity, and electrification, reinforcing the long-term growth and defensive characteristics of the infrastructure asset class.

Technology & Communications

Middlefield Fund Tickers & Codes: MINN / SIH.UN / MID 925 / MDIV

by Shane Obata, Portfolio Manager

Despite near-term market volatility, the fundamental growth drivers of the Technology sector continue to present the strongest risk-adjusted opportunity in today’s market. Looking at consensus bottom-up projections, Info Tech is slated for a staggering 45% EPS growth in 2026 and 25% in 2027. To put that in perspective, that is more than double the expected growth of the broader S&P 500 this year. You simply cannot afford to ignore those fundamentals, but you also can’t afford to passively invest in the sector blindly. The rising tide that once lifted all technology stocks has receded; investors are now drawing sharp distinctions among companies that execute and those that do not.

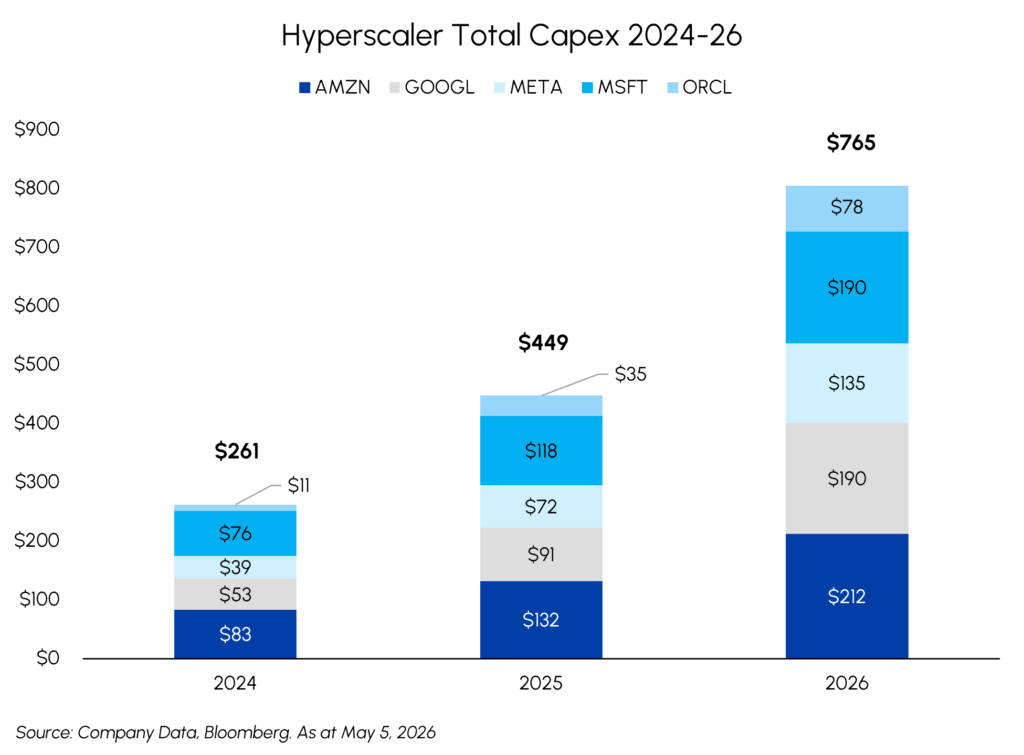

Alongside the massive CapEx announcements, we are now seeing tangible ROI from the largest hyperscalers. The “bubble” narrative starts to fall apart when witnessing Google Cloud’s revenue surge and Amazon AWS’ strongest growth since 2022. This isn’t speculative, it’s an infrastructure land invesment. Crucially, capacity has become the ultimate differentiator. Demand for compute is currently lapping supply at a pace that keeps users constantly rate-limited. The companies that own the “physicality” of AI, including the data centers and the underlying hardware, hold massive structural leverage. This reinforces why our Innovation strategies have pivoted toward these tangible beneficiaries.

However, the real alpha is no longer found solely in the crowded trades on the Nasdaq. Our research is increasingly focused on the “Silicon Shield” in Asia. For the average North American investor, high-conviction stories in Japan, South Korea, and Taiwan are notoriously difficult to access due to a lack of options beyond local listings. Many of these firms provide mission-critical inputs into the AI supply chain, yet they remain largely off the radar of domestic retail flows. Our mandates bridge this gap, providing exposure to the specialized, hard-to-reach corners of the global tech stack that are actually powering the buildout.

Our core investment themes haven’t changed because the fundamental reality hasn’t changed. We used the recent volatility, including the nerves surrounding geopolitical tensions, as an opportunity to tactically add to our favorite themes/names. While the “Magnificent Seven” stocks have been a crowded trade, we continue to find the most exciting growth in the foundational layers of the industry. The disparity in this market is high, but for active managers, that is exactly where the opportunity lies.

Resources

Middlefield Fund Tickers & Codes: MID 800 / MID 161 / MID 265 / MRF FT LP / Discovery FT LP

by Dennis da Silva, Senior Portfolio Manager

Energy remained the dominant driver across resource markets in April, while gold lagged broader equities for a second consecutive month. Gold declined modestly and underperformed gold equities, as competing forces of geopolitical demand and macro headwinds created a choppy backdrop. While elevated oil prices continue to support gold’s role as an inflation hedge, higher yields and delayed rate cut expectations have capped near-term upside. Despite this, the longer-term bull thesis remains intact, underpinned by structural factors including rising global debt levels and persistent geopolitical uncertainty.

Asia has been the epicenter of the energy crisis, implementing severe demand measures. The Iran war continues to choke off critical natural gas supply to Europe and Asia, with TTF and Asian spot prices up approximately 40% since the start of the war. Throughout this period, Henry Hub prices have fallen approximately 10% reflecting the relative supply security in North American markets and the divergent effects of the standstill in the Strait of Hormuz. The ActivEnergy Dividend Class ETF (MAEC) returned 3.65% during April outpacing the S&P/TSX Capped Energy Index return of 1.4%.

Geopolitical uncertainty in the Middle East has renewed global focus on energy security, elevating the strategic value of reliable, non-OPEC supply — an area where Canada is exceptionally well-positioned. Concurrently, the Carney government’s policy agenda — centered on accelerated project approvals, export diversification, and an explicit ambition to establish Canada as an energy superpower — creates a rare alignment of near-term market tailwinds and long-term structural support. Federal commitment to transformative infrastructure, including LNG Canada Phase 2, Ksi Lisims LNG, the North Coast Transmission Line and the Pathways Alliance carbon-capture hub, reinforces that policy intent with capital and execution.

Shell’s $22 billion acquisition of ARC Resources makes them the largest LNG player in Canada and the 3rd largest Montney producer. Management described it as an opportunistic, liquids-driven deal and signaled strong provincial and federal support for an LNG Canada Phase 2 sanction. With that context, we believe Tourmaline is undervalued relative to the ARC transaction metrics and see $80/share as fair value. Reuters has also reported that Total, ConocoPhillips, Equinor, and BP are all taking a fresh look at Canadian peers, with Apollo, Blackstone, and KKR eyeing a stake in LNG Canada valued at $10–15 billion in addition to other Canadian energy infrastructure. Reserve Life Indices for European supermajors continue to decline with Shell & BP well below 10 years, which reinforce the thesis that M&A will be required by these entities to improve asset duration.

Exchange Traded Funds (ETFs)

Mutual Funds (FE | F)

TSX-Listed Closed-End Funds

| Fund | Ticker | Strategy |

|---|---|---|

| MINT Income Fund | MID.UN | Equity Income |

| Sustainable Innovation & Health Dividend Fund | SIH.UN | Innovation & Healthcare |

TSX-Listed Split Share Corps. (Class A | Preferred)

| Fund | Ticker | Strategy |

|---|---|---|

| E-Split Corp. | ENS | ENS.PR.A | Energy Infrastructure |

| Real Estate Split Corp. | RS | RS.PR.A | Real Estate |

| Infrastructure Dividend Split Corp. | IS | IS.PR.A | Infrastructure |

LSE-Listed Fund

| Fund | Ticker | Strategy |

|---|---|---|

| Middlefield Canadian Enhanced Income UCITS ETF | LSE: MCTC | LSE: MCTP | Canadian Equity Income |

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments, including ETFs. Please read the prospectus before investing. You will usually pay brokerage fees to your dealer if you purchase or sell units/shares of investment funds on the Toronto Stock Exchange or other alternative Canadian trading system (an “Exchange”). If the units/shares are purchased or sold on an Exchange, investors may pay more than the current net asset value when buying and may receive less than the current net asset value when selling them. There are ongoing fees and expenses associated with owning units or shares of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in these documents. Mutual funds and investment funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain statements in this disclosure are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may”, “will”, “should”, “could”, “expect”, “anticipate”, “intend”, “plan”, “believe”, or “estimate”, or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what Middlefield Funds and the portfolio manager believe to be reasonable assumptions, neither Middlefield Funds nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

This material has been prepared for informational purposes only without regard to any particular user’s investment objectives or financial situation. This communication constitutes neither a recommendation to enter into a particular transaction nor a representation that any product described herein is suitable or appropriate for you. Investment decisions should be made with guidance from a qualified professional. The opinions contained in this report are solely those of Middlefield Limited (“ML”) and are subject to change without notice. ML makes every effort to ensure that the information has been derived from sources believed to reliable, but we cannot represent that they are complete or accurate. However, ML assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. ML is under no obligation to update the information contained herein. This document is not to be construed as a solicitation, recommendation or offer to buy or sell any security, financial product or instrument.