Index

Macro Update

by Dean Orrico, President & CEO and Robert Lauzon, CIO

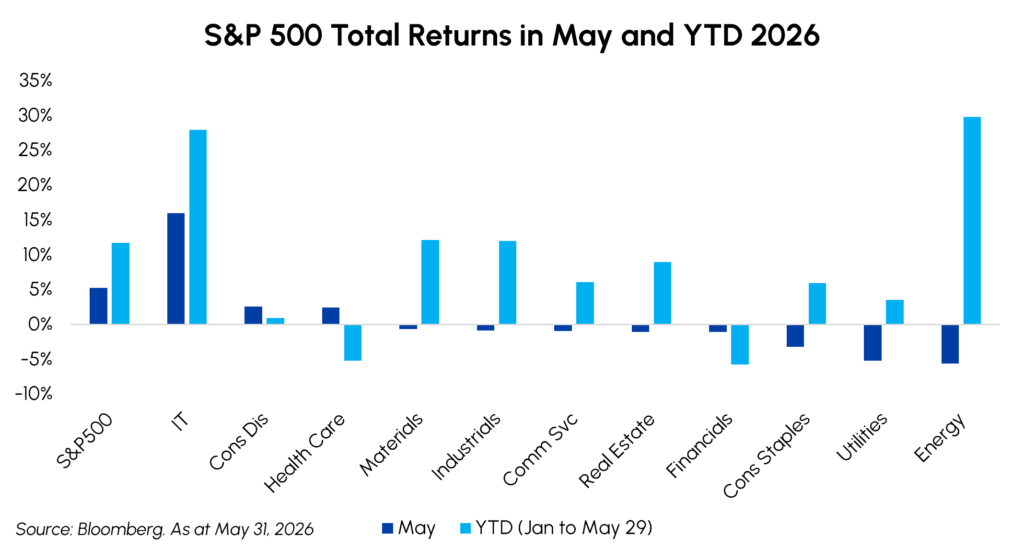

Global equity markets continued to grind higher in May, with the S&P 500 returning 5.3% to close at an all-time high following a historic 8-week winning streak. The TSX Composite returned 2.5%, landing just shy of its own record peak marking its second consecutive monthly advance, with earnings proving to be driving force behind the sustained rally. While broader market sentiment was heavily influenced by fluctuating geopolitical tensions and macro shifts, distinct sectors emerged as clear leaders and laggards. Global oil balances are structurally tight and under immediate pressure from critically low commercial inventories, fading strategic reserves, and a potential near-term spike in crude as summer demand peaks. We remain intensely focused on the closure of the Strait and even after it reopens, a complex bottleneck of mine removal, infrastructure repair, and logistics reconfiguration means normal supply flows will not recover until year-end. Consequently, we expect energy prices to remain higher for longer with a structurally elevated price floor, driven by multi-billion-dollar infrastructure repair costs and a global mandate for nations to permanently hold higher baseline inventories. Although the June 5th sell-off was notable and potentially the beginning of some choppy market action given stretched positioning into a slew of near-term mega-cap IPOs, we view it as a healthy reset within an earnings led bull market.

The S&P 500 Technology sector surged +16.0% in May, with parabolic moves concentrated across the AI infrastructure landscape. The top 10 performing stocks in the S&P 500 were mostly hardware, memory, or cybersecurity names, representing the physical backbone of the data center buildout. We remain constructive on the secular AI theme and have been positioned to take advantage of anticipated strength across the entire value chain including chips, data centers, power, and materials across multiple strategies.

The AI boom is being funded by equity and debt markets as well as government stakes being considered. The upcoming blockbuster IPOs of SpaceX, Anthropic, and OpenAI are expected to raise a total of $200B over the next few months. Concurrently, Alphabet also announced a massive $80B equity issuance, while Meta is also considering a raise in the range of “tens of billions”. The pace of equity supply from mega cap Tech companies has begun to fuel debate around whether the market faces a structural supply shock. While we think the AI theme is durable, we remain disciplined and believe better entry points may emerge throughout the summer.

On the policy front, Kevin Warsh’s inaugural FOMC meeting as Fed Chair approaches in mid-June, amid ongoing debates over the best course of action. Despite vocal political pressure from the White House for immediate interest rate cuts, we anticipate the Fed will remain firmly on hold for the foreseeable future, given sticky inflation and a resilient domestic economy. Meanwhile in Canada, substantial infrastructure investments paired with slowing population growth are expected to finally reverse a decade of lackluster Canadian productivity, improve per-capita metrics, and create a healthier long-term corporate environment.

Fixed Income

Middlefield Fund Tickers & Codes: MSBP / MID 435

by Gordon McKay, Senior Portfolio Manager

May’s positive returns were driven by continued income harvesting, alongside falling front-end interest rates in Canada and tightening credit spreads. MSBP selectively participated in several new issues during the month, taking advantage of attractive pricing for some first-time issuers, including Alphabet’s historic inaugural issue into the Canadian Maple bond market. As rates and spreads fell, the Fund modestly reduced its duration to 1.15 years. The currency adjusted yield to maturity held steady at 3.72%.

There is an opportunity in short-duration credit to enhance returns by maximizing exposure to embedded upside options. Tilting the portfolio towards bonds trading below their call price allows for upside surprises. MSBP realized one of these upside surprises in May when a portion of its Medline Inc. 6.25% 2029 bonds was called early.

Medline Inc. is the largest distributor of medical-surgical products in the U.S. by net sales. After being taken private in 2021, the company went public again in the largest IPO in 2025. Most of the proceeds were used to reduce debt, with management focused on driving net leverage below its 3.0x target. In addition to being the first maturing bond in their capital structure, the 6.25% notes due in 2029 were first-lien secured and rated investment grade. The loan-to-value through the secured debt was a conservative 20%. MSBP purchased the bonds in mid-March at a price of $102.40. At the time, the yield-to-worst was 5.00%, the yield-to-maturity was 5.38%, and the current yield was 6.10% – offering a strong range of expected returns before embedded options. In May, a third of those bonds were called at a price of $103.125, delivering an annualized return of 10.13% on that portion. Selecting high quality bonds with embedded options allows the Fund to enhance returns without adding risk.

Real Estate

Middlefield Fund Tickers & Codes: MREL / MID 600 / RS / RS.PR.A

by Dean Orrico, President & CEO

The US Real Estate sector pulled back by 1.05% in May while the Canadian Real Estate sector eked out a gain of 0.57%. Both underperformed the broader markets, largely due to shifting interest rate expectations as long-term Treasury yields surged during the month. More specifically, the 30-year US yield breached 5% early in the month and climbed to its highest level since 2007, touching 5.19% on May 19 before retreating in the last week of May. Yield was still marginally higher in the month and the expectations for Federal Reserve rate cuts have dimmed in the face of entrenched inflation and a stable economy. Since REITs are more rate-sensitive (valued largely on yield spreads employing debt financing), rising long-end yields compress valuations and increase borrowing costs. Notwithstanding the headwind of higher longer dated government yields, the Canadian REIT sector has generated a YTD total return exceeding 9% as at the end of May, reflecting the continued solid fundamentals across most real estate subsectors.

In the US, Data Center REITs were the standout performers as demand for AI infrastructure continued to drive leasing activity and investor interest. Retail REITs were the only sub-sector to post a negative return in May with Simon Property Group, one of the largest players, posting earnings miss. In Canada, Real Estate Services lagged the market with a 3.2% loss, while Retail REITs, unlike their US counterpart, led with a 3.2% advance. This reflects the solid fundamentals in the grocery-anchored and necessity-based retail sector, supported by defensive demand in an uncertain macro environment.

The Middlefield Real Estate Dividend ETF delivered a 0.95% return in May and 9.6% YTD, exceeding the Canadian REIT benchmark and in line with the more global Morningstar benchmark. Extendicare was again a clear standout in the senior housing subsector, advancing another 8.2% on top of its 13.9% surge the previous month. Extendicare reported quarterly revenue and earnings that beat consensus estimates, prompting analysts to raise their target prices in anticipation of the company’s addition to the S&P/TSX Composite Index on June 22. Extendicare exemplifies our conviction in investment ideas outside the benchmark. We remain structurally positive on seniors housing, supported by constrained supply and accelerating demographic demand.

Two of our residential REITS also positively contributed to performance in May for different reasons. Canadian Apartment REIT (CAPREIT) was down by approximately 4% as the company cut estimates. It is a big weight in the benchmark, and our prudent underweight position was a contributor to our relative outperformance. On the other hand, our overweight in Killam Apartment REIT was a top contributor as it gained approximately +7.8% in May, driven by a combination of solid Q1 results, positive operating momentum, and broad analyst upgrades. Killam’s concentration in Atlantic Canada, particularly Halifax, sets it apart from peers exposed to the weaker Ontario and BC markets that weighed on CAPREIT.

Healthcare

Middlefield Fund Tickers & Codes: MHCD / MID 325 / SIH.UN

by Dean Orrico, President & CEO

Healthcare had a strong month, with the broad sector gaining roughly 2.5% as most of our core areas participated. Pharmaceuticals led the way, up nearly 7%, with life science tools and managed care close behind. On the policy front, the abrupt resignation of FDA Commissioner Marty Makary grabbed headlines and introduced some near-term uncertainty around the agency’s leadership. We read his departure as a modest positive as his tenure had been marked by friction with the administration and mixed signals on where the FDA was setting the bar for approving new drugs. The administration’s clear preference for a faster, more approval-friendly FDA leaves us comfortable that his successor will likely be aligned with a pro-innovation agenda, a constructive setup for the pipeline-driven names we own.

Last month was a heavy one for medical conferences, headlined by ASCO — the premier cancer research conference. The news flow was encouraging for our large-cap pharma holdings. Across the board, we saw positive data for the next wave of cancer therapies to drive growth later this decade. Johnson & Johnson stood out with strong results for a key blood-cancer drug that should cement its leadership in that market, while Merck and Pfizer both advanced promising new lung-cancer treatments. Importantly, these readouts speak to a broader theme we’ve emphasized: big pharma is steadily building out its next generation of products to offset the patent expirations on the horizon, and the early evidence suggests that effort is on track.

The other major event was ADA, the leading annual diabetes conference. The spotlight was on Eli Lilly, our largest holding, which presented data that in our view further extends its already commanding lead. Lilly’s next obesity drug, retatrutide, delivered weight loss approaching 30%, a level that rivals bariatric surgery and sets a new bar for the industry. A lower dose of the same drug proved nearly as effective as today’s leading treatments but was far more user-friendly for patients, opening the door to a far wider group of potential users. Lilly also showcased a second promising pipeline drug, eloralintide, which pairs strong weight loss with notably fewer side effects. With these two products slated to launch in 2027 and 2028, we believe Lilly is well positioned to stay several steps ahead of the competition.

Infrastructure & Resources

Middlefield Fund Tickers & Codes: MINF / MID 265 / MID 510 / ENS / IS / IS.PR.A / MID 800 / MID 161 / MID 265 / MRF FT LP / Discovery FT LP

by Robert Lauzon, CIO and Dennis da Silva, Senior Portfolio Manager

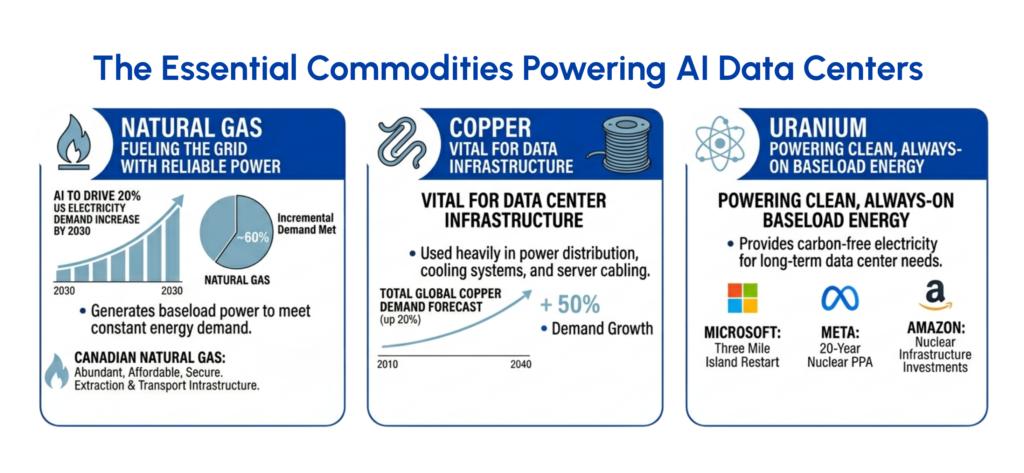

The scale of the AI infrastructure buildout is accelerating at a rapid pace, and its impact is being felt beyond just the technology sector. The largest bottleneck to the AI buildout remains power, with several commodities and critical minerals playing a key role, including natural gas, copper, and uranium.

Goldman Sachs projects AI will drive a 20% increase in U.S. electricity demand by 2030 and estimates that natural gas will meet roughly 60% of that incremental demand, ranking it alongside LNG export growth as one of the most consequential demand drivers for natural gas this decade. Data centers require constant power, something which renewables alone cannot reliably guarantee. Canadian natural gas stands out given its availability and affordability, particularly at a time when geopolitical disruptions have caused European natural gas prices to rise sharply. Canada remains a secure, reliable supplier of natural gas given its abundance and existing infrastructure to extract and transport across regions and continents.

A single hyperscale AI data center campus can require up to 50,000 tonnes of copper across power distribution, cooling, and server infrastructure. As hundreds of gigawatts of AI-related capacity is built out globally, copper remains one of the most constrained inputs in the system. The structural bull case for copper extends well beyond AI, with total global copper demand forecast to grow 50% by 2040 as grid modernization, EV adoption, and electrification compound the AI-driven tailwind. With average mining projects taking a decade or more from discovery to production, supply can’t respond quickly, creating a prolonged repricing opportunity for copper producers and developers.

Uranium serves as the long-duration, clean baseload option for large tech companies that aim to meet both reliability and sustainability commitments. Microsoft’s contracted restart of Three Mile Island, Meta’s 20-year nuclear power purchase agreement, and Amazon’s multi-billion-dollar nuclear infrastructure investments showcase the long-duration offtake commitments that directly underpin uranium demand for decades.

Together, these commodities represent the foundation of the AI infrastructure buildout, and we are participating in this theme within our infrastructure and diversified funds through several complementary angles. On the natural gas side, Enbridge and TC Energy are benefiting from rising volume growth tied to data center power demand, as well as commercial and residential usage across North America. Tourmaline, Canada’s largest natural gas producer, is positioned to supply the volumes that will flow through these expanding pipelines toward domestic data center demand load and growing LNG export markets. Our flow-through partnerships provide additional exposure to the copper and uranium side of the theme, where the investment case for miners and developers remains durable and underappreciated relative to the scale of the demand that lies ahead.

Technology & Communications

Middlefield Fund Tickers & Codes: MINN / SIH.UN / MID 925 / MDIV

by Shane Obata, Portfolio Manager

Technology remains the center of the equity market’s earnings story. While investors have been quick to debate valuations, positioning and short-term volatility, the more important point is that earnings momentum remains firmly supportive. Alongside Energy, Technology has been one of the clearest drivers of positive earnings revisions, reinforcing our view that the sector continues to offer some of the strongest risk-adjusted opportunities in the market.

The early June volatility should be viewed in that context. We see it as a healthy reset rather than a warning sign that the AI buildout is losing momentum. After a powerful move in many AI-related stocks, some digestion was inevitable. But the fundamental backdrop remains intact: hyperscalers continue to invest aggressively, demand for compute remains supply constrained, and the AI infrastructure cycle is still broadening across semiconductors, memory, networking, power and advanced materials. In our view, volatility is creating a more attractive entry point for active managers, not undermining the core thesis. Recent developments in Asia reinforce that point. Jensen Huang’s latest visit to Korea again highlighted how global and hardware-intensive the AI buildout has become. NVIDIA announced partnerships across the Korean ecosystem, with a focus on advanced memory, AI factories, data centers, robotics and physical AI infrastructure.

That is exactly why our Technology exposure is not simply a U.S. mega-cap story. NVIDIA remains central to AI, but the opportunity set extends across the broader supply chain. Memory, substrates, advanced packaging, optics, electrical equipment and other mission-critical inputs are increasingly concentrated in Asia. Korea, Japan and Taiwan remain essential to enabling the next phase of AI infrastructure, which supports our continued overweight to Asia versus Europe.

The key message for investors is simple: the AI trade is maturing, not ending. The next stage will likely reward selectivity, supply-chain depth and earnings delivery rather than broad exposure to anything with an AI label. Technology remains a high conviction sector because the earnings revision cycle is positive, the AI buildout remains well funded, and the most attractive opportunities are increasingly found in the companies powering the infrastructure beneath the headline applications.

Exchange Traded Funds (ETFs)

Mutual Funds (FE | F)

TSX-Listed Closed-End Funds

| Fund | Ticker | Strategy |

|---|---|---|

| MINT Income Fund | MID.UN | Equity Income |

| Sustainable Innovation & Health Dividend Fund | SIH.UN | Innovation & Healthcare |

TSX-Listed Split Share Corps. (Class A | Preferred)

| Fund | Ticker | Strategy |

|---|---|---|

| E-Split Corp. | ENS | ENS.PR.A | Energy Infrastructure |

| Real Estate Split Corp. | RS | RS.PR.A | Real Estate |

| Infrastructure Dividend Split Corp. | IS | IS.PR.A | Infrastructure |

LSE-Listed Fund

| Fund | Ticker | Strategy |

|---|---|---|

| Middlefield Canadian Enhanced Income UCITS ETF | LSE: MCTC | LSE: MCTP | Canadian Equity Income |

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments, including ETFs. Please read the prospectus before investing. You will usually pay brokerage fees to your dealer if you purchase or sell units/shares of investment funds on the Toronto Stock Exchange or other alternative Canadian trading system (an “Exchange”). If the units/shares are purchased or sold on an Exchange, investors may pay more than the current net asset value when buying and may receive less than the current net asset value when selling them. There are ongoing fees and expenses associated with owning units or shares of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in these documents. Mutual funds and investment funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain statements in this disclosure are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may”, “will”, “should”, “could”, “expect”, “anticipate”, “intend”, “plan”, “believe”, or “estimate”, or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what Middlefield Funds and the portfolio manager believe to be reasonable assumptions, neither Middlefield Funds nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

This material has been prepared for informational purposes only without regard to any particular user’s investment objectives or financial situation. This communication constitutes neither a recommendation to enter into a particular transaction nor a representation that any product described herein is suitable or appropriate for you. Investment decisions should be made with guidance from a qualified professional. The opinions contained in this report are solely those of Middlefield Limited (“ML”) and are subject to change without notice. ML makes every effort to ensure that the information has been derived from sources believed to reliable, but we cannot represent that they are complete or accurate. However, ML assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. ML is under no obligation to update the information contained herein. This document is not to be construed as a solicitation, recommendation or offer to buy or sell any security, financial product or instrument.