Index

Overview

The real estate sector is comprised of many different property types, each with unique characteristics. Investors can access this diverse sector by investing in properties directly or through publicly-listed real estate companies which are most commonly structured as real estate investment trusts (REITs). It’s important to note that as long as REITs comply with certain provisions, they are not taxed on the income and gains generated in the trust, but instead flow these out to their unitholders. If an investor holds a REIT in a tax-exempt vehicle such as an RRSP, tax on the distributions can be deferred until the investment is withdrawn.

Public REITs own, operate or finance income-generating portfolios of real estate assets. In fact, they were initially established in the U.S. to provide “all investors” with the opportunity to invest in real estate assets, something that was previously available only to wealthy investors. As a result, they are issued by prospectus, trade on a stock exchange and are suitable for a wide range of investors and investment sizes. More specifically, public REIT investors are not subject to restrictive eligibility requirements, minimum investment sizes or upfront costs. In addition, because they are issued by a prospectus approved by securities regulators they have greater regulatory oversight and receive more third-party scrutiny from stock analysts and institutional investors. Since public REITs trade on exchanges, they are extremely liquid and easy to access.

Large and sophisticated institutional investors have been investing in real estate for many decades due to its attractive income streams and lower correlations with conventional asset classes. More recently, institutional investors have been supplementing their exposure to private real estate with publicly traded REITs due to the increasing quality of the publicly traded REIT sector, their attractive valuations and better liquidity. Public REITs are also becoming frequent takeover targets of pensions and other large asset managers. In Canada, we’ve seen a number of takeover transactions including Blackstone’s acquisition of Pure Industrial Real Estate Trust in 2018 and WPT REIT in 2021 as well as the announcement in November 2022 by Dream Industrial REIT and GIC (sovereign wealth fund in Singapore) to acquire Summit Industrial Income REIT.

Source: Refinitiv. As at December 31, 2022. Canadian REITs: S&P/TSX Real Estate Sector Canadian Bonds: S&P Canadian Aggregate Bond Index |

Real Estate Sub-Sectors

Traditional Property Types

Industrial

- What is it? Warehousing, logistics and manufacturing space

- What impacts demand: Onshoring trends, inventory management systems shifting from just-in-time to just-in-case and the proliferation of e-commerce

- Outlook: Robust rent growth driven by significant supply/demand imbalance

Multi-Family

- What is it? Purpose-built rental apartments

- What impacts demand: Record immigration targets and homebuyers being priced out of the housing market

- Outlook: Sustained growth in apartment rents and occupancy until supply can meet the growing demand for housing

Retail

- What is it? Properties used to sell consumer goods and services

- What impacts demand? Amenity-rich ecosystems with high foot traffic and mixed-use development upside

- Outlook: Investors concentrating on grocery anchored centres or urban properties with mixed-use / re-development potential

Office

- What is it? Office space located primarily in central business districts

- What impacts demand: General economic activity and employees returning to the office

- Outlook: Uncertain outlook due to the high number of employees working from home

Healthcare

- What is it? Hospitals, clinics and seniors housing facilities

- What impacts demand: Demographic trends such as an aging population and the emergence of outpatient and in-home healthcare access

- Outlook: Defensive asset class with a stable cash flow profile being supported by occupancy recovering from the pandemic

Emerging Property Types

Towers

- What is it? Communications towers that host cellular network broadcast equipment

- What impacts demand: Growth in mobile data traffic and the expansion of wireless networks such as the ongoing build-out of 5G

- Outlook: Positive as more people use smartphones and other mobile devices that require investments in connectivity

Data Centers

- What is it? Specialized facilities used to store, process and manage data

- What impacts demand: Increased reliance on digital technologies and increasing demand for data storage and processing capacity

- Outlook: Attractive industry trends but growing competition requires careful security selection

Self-Storage

- What is it? Facilities that provide rental storage space for individuals and businesses

- What impacts demand: The rise of e-commerce and more people renting or downsizing their homes creates the need for extra storage space

- Outlook: Stable outlook in a defensive asset class that is less sensitive to interest rate fluctuations and the economic cycle

Manufactured Housing Communities

- What is it? Communities of modular homes that share common amenities

- What impacts demand: Growing popularity of low-maintenance housing options among retirees and affordable housing solutions for middleclass families

- Outlook: Defensive asset class with a positive outlook as the population ages and more families seek affordable housing options

Life Science Office

- What is it? Offices, research laboratories and drug manufacturing facilities

- What impacts demand: Specific needs of life science R&D such as sterilized rooms, collaboration space and unique temperature control requirements

- Outlook: Positive long-term outlook as biopharma companies, academic centers and government institutions continue to invest in life science research

Real Estate Equity: Advantages

Tax Advantaged Income

REITs have the potential for sustainable income and competitive total returns. They are among the most tax-efficient sources of income for investors. Due to their unique structure, since REITs are required to distribute at least 90% of their taxable income to investors in the form of distributions, REITs typically do not pay corporate income taxes. Avoiding taxation at the corporate level leaves more distributable income for investors and results in attractive dividend yields. Moreover, since REITs are distributing a significant level of their free cash flow to investors, they do not engage in as much development activity which often carries higher levels risk since development can be an expensive, lengthy and complicated. Income generated from real estate tends to be higher than the dividends received from other equities.

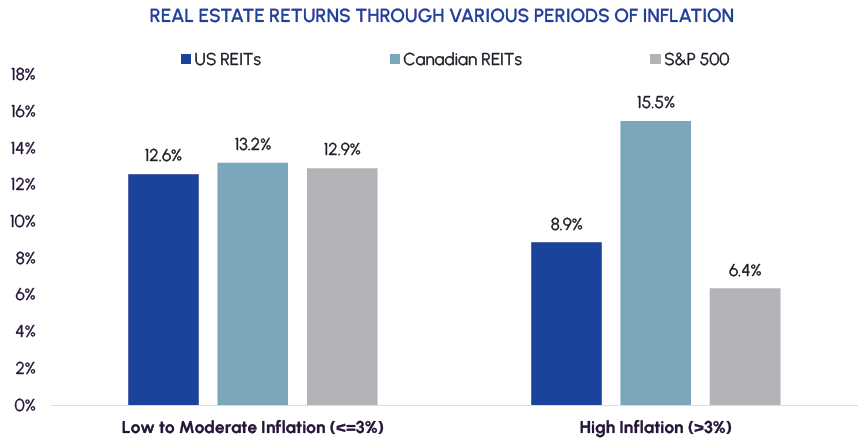

Inflation Hedge

Investing in real estate can serve as a useful hedge against inflation. Many leases include inflation-linked rent escalators and landlords can pass on higher costs by raising rents. Rents are growing at a record pace within certain asset classes including multi-family apartments and industrial warehouses. Property prices also tend to rise with inflation over the long-term.

Source: Bloomberg. December 31, 2002 to December 31, 2022 Source: Bloomberg. December 31, 2002 to December 31, 2022 |

Stable and Defensive Earnings

REITs possess defensive characteristics. Their revenues are secured by long-term leases which provide predictable revenue streams, even under challenging economic conditions. Many of the operating expenses for the properties they own, such as utility bills, are borne by tenants which provides margin protection. This has resulted in consistent earnings growth over time and has also supported dividend growth. The FTSE NAREIT ALL REITs Index had an average annual dividend growth rate of 6.6% for the period of 1994 to 2020.

Access to a High-Barrier Asset Class

Direct ownership of real estate is expensive and complicated. Commercial properties often cost hundreds of millions of dollars to develop and require specialized capabilities to navigate zoning, title transfers, building maintenance, property management etc. As a result, these assets are often concentrated in the hands of large, institutional investors with real estate expertise. REITs offer an excellent solution to these high barriers to entry as they are liquid, professionally managed publicly-traded securities with no minimum investment requirements.

Diversification

Real Estate is typically uncorrelated with fixed income investments and can be a valuable source of diversification. This can help lower overall risk and increase potential returns across portfolio.

|

10-Year Monthly Correlations between Global REITs and Fixed Income |

|

| Asset Class | Correlation to Global REITs |

|---|---|

| S&P Global REIT Index |

1 |

| S&P US Aggregate Bond Index | 0.49 |

| S&P CAD Aggregate Bond Index |

0.523 |

| Source: Bloomberg. As at December 31, 2022 | |

Middlefield’s Real Estate Solutions

Middlefield’s real estate strategies are designed for investors seeking income and growth from a portfolio of large-cap companies diversified across the global real estate sector. Middlefield’s history in real estate began when the firm was founded over 40 years ago and we have been managing dedicated REIT strategies for over 10 years. Our solutions provide Canadian investors with global exposure to a sector that has attractive defensive and inflation-protection attributes. Middlefield’s real estate funds have won multiple awards in the real estate sector.

| Strategy | Fund Structure | Ticker/Fund Code | Investment Focus | Risk Rating |

|---|---|---|---|---|

| Middlefield Real Estate Dividend ETF | ETF | TSX: MREL | Diversified Global Real Estate |

Medium |

| Middlefield Real Estate Dividend Class | Mutual Fund |

F Series: MID 601 |

Diversified Global Real Estate |

Medium |

| Middlefield Real Estate Split Corp. | Split Share |

Preferred Shares: RS.PR.A |

15-20 high conviction REITs |

Medium |

Income

All Middlefield real estate funds provide investors with attractive levels of monthly income.

Holdings

Middlefield’s real estate strategies are actively managed portfolios holding approximately 30 to 45 names. We focus on REITs that generate stable operating income, carry low leverage and pay growing levels of dividends.

|

Disclaimer

This material has been prepared for informational purposes only without regard to any particular user’s investment objectives or financial situation. This communication constitutes neither a recommendation to enter into a particular transaction nor a representation that any product described herein is suitable or appropriate for you. Investment decisions should be made with guidance from a qualified professional. The opinions contained in this report are solely those of Middlefield Limited (“ML”) and are subject to change without notice. ML makes every effort to ensure that the information has been derived from sources believed to reliable, but we cannot represent that they are complete or accurate. However, ML assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. ML is under no obligation to update the information contained herein. This document is not to be construed as a solicitation, recommendation or offer to buy or sell any security, financial product or instrument.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund and ETF investments. Please read the prospectus and publicly filed documents before investing. Mutual funds and ETFs are not guaranteed, their values

change frequently, and past performance may not be repeated. You will usually pay brokerage fees to your dealer if you purchase or sell shares of an investment fund on the Toronto Stock Exchange or alternative Canadian trading platform (an “exchange”). If the shares are purchased or sold on an exchange, investors may pay more than the current net asset value when buying shares of the investment fund and may receive less than the current net asset value when selling them. There are ongoing fees and expenses associated with owning shares of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in the public filings available at www.sedar.com. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Certain statements in this press release may be viewed as forward-looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, intentions, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects”, “is expected”, “anticipates”, “plans”, “estimates” or “intends” (or negative or grammatical variations thereof), or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and may be forward-looking statements. Forward-looking statements are subject to a variety of risks and uncertainties which could cause actual events or results to differ from those reflected in the forward-looking statements including as a result of changes in the general economic and political environment, changes in applicable legislation, and the performance of each fund. There are no assurances the funds can fulfill such forward-looking statements and the funds do not undertake any obligation to update such statements. Such forward-looking statements are only predictions; actual events or results may differ materially as a result of risks facing one or more of the funds, many of which are beyond the control of the funds.