Index

Macro Update

by Dean Orrico, President & CEO and Robert Lauzon, CIO

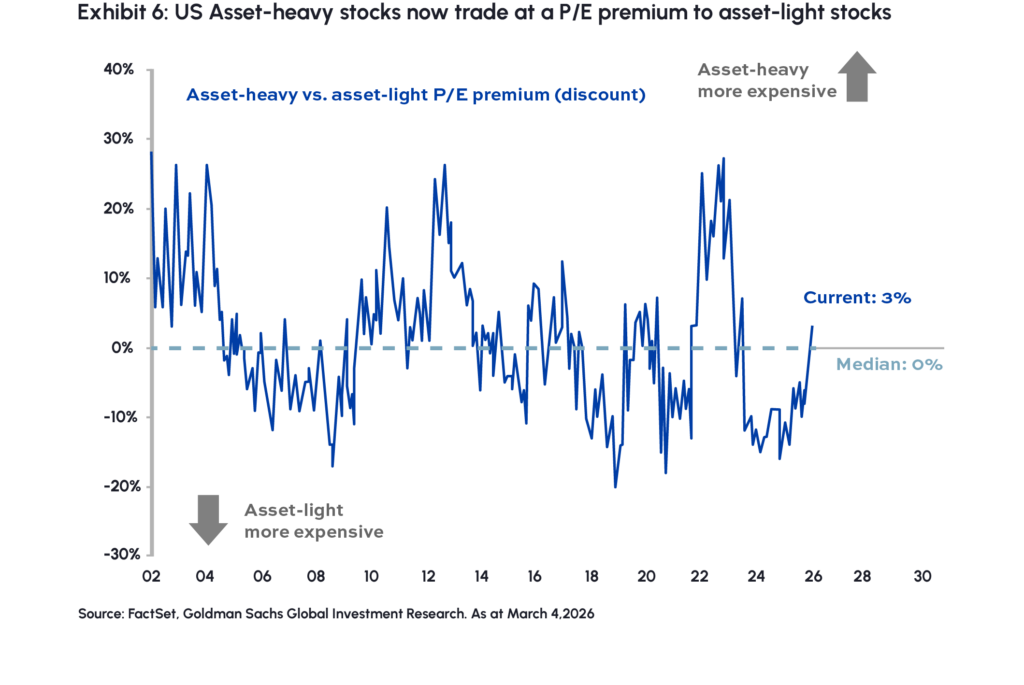

February extended the market broadening theme that has been developing since late 2025, with the TSX Composite (+7.7%) continuing to outperform the S&P 500 (-0.7%) and the Nasdaq (-3.3%) as at the end of February 2026. While major indices remain in a bull market, rising single-stock volatility has triggered significant sector rotation, particularly out of Mega-Cap Technology and into “HALO” sectors (high assets, low obsolescence), including Energy, Utilities and Pipelines, Materials and Real Estate.

The market digested the U.S. Supreme Court’s decision to overrule the Trump administration’s IEEPA tariff framework in stride. President Trump announced a revised policy imposing a 10% flat tariff under Section 122, with plans to increase the rate to 15% shortly thereafter. Due to existing exemptions, the effective tariff rate falls to 12.1%, compared to 13.6% prior to the ruling. Section 122 allows the administration to maintain this tariff structure for up to 150 days, while additional measures, including country-specific investigations under Section 301, remain the probable path forward. Although uncertainty persists around the future of the USMCA trade agreement, Canadian PM Mark Carney continued advancing trade diversification efforts, announcing multi-billion-dollar agreements with Australia and India in the past few weeks focused on critical minerals, defense, and artificial intelligence.

The market digested the U.S. Supreme Court’s decision to overrule the Trump administration’s IEEPA tariff framework in stride. President Trump announced a revised policy imposing a 10% flat tariff under Section 122, with plans to increase the rate to 15% shortly thereafter. Due to existing exemptions, the effective tariff rate falls to 12.1%, compared to 13.6% prior to the ruling. Section 122 allows the administration to maintain this tariff structure for up to 150 days, while additional measures, including country-specific investigations under Section 301, remain the probable path forward. Although uncertainty persists around the future of the USMCA trade agreement, Canadian PM Mark Carney continued advancing trade diversification efforts, announcing multi-billion-dollar agreements with Australia and India in the past few weeks focused on critical minerals, defense, and artificial intelligence.

Markets were incredibly resilient during the opening week of the Iran war as investors anticipated a relatively brief conflict. However, as Operation Epic Fury enters its second week, the market is now pricing in a higher probability of a protracted conflict. Oil prices crossing the $100/bbl threshold early this week was the catalyst precipitating a higher risk premium embedded into both valuations of global equities and yields as inflation fears escalate and the level of earnings growth for 2026 is questioned. The problem is that it’s not just geopolitical tensions that equities are grappling with – the two other potentially more significant headwinds include the AI narrative losing its persuasive power as hyperscalers get penalized for massive capital expenditures while the sustainability of data center spending and disruption worries have upended multiple sectors (software, data providers, financials) and private credit – where redemptions seem to be relentlessly mounting across the board placing pressure on the entire industry.

Our view is the headwinds created by the Strait of Hormuz being effectively closed will cause enough extreme short-term market turmoil that Washington will start looking more vigorously for exit ramps. In the meantime, the backdrop of the “fog of war” will cause investors to position more defensively in sectors with more resilient income streams, lower volatility and exposure to needs-based industries such as our Short Duration Bond Plus, ActivEnergy, Income Plus and Real Estate and Healthcare strategies.

Fixed Income

Middlefield Fund Tickers & Codes: MSBP / MID 435

by Gordon McKay, Senior Portfolio Manager

Interest rates declined sharply in both the U.S. and Canada during February. While there was some economic justification for lower rates, most notably subdued inflation readings in both countries and weak employment data in Canada, rising uncertainty was likely the dominant driver. The U.S. Supreme Court’s decision to overrule the Trump administration’s IEEPA tariff framework added volatility to a sanguine risk market. In addition, new AI features and use cases, along with an alarmist article about the future of software businesses and white-collar workers, added to market fears about how disruptive AI might be to both business and workers’ future earnings.

Credit spreads moved wider in the uncertainty. In the U.S. (the most liquid credit market), investment grade spreads widened 11 basis points (“bps”) while high yield backed up 24 bps. Credit initially tightened following the tariff ruling, as investors anticipated refunds for tariffs already collected. That move quickly reversed when the administration announced new tariffs under a separate authority. Public credit came under pressure because of the issues in private credit and syndicated term loans, related asset classes. Investors fear higher exposure to the software sector in the loan and private credit portfolios could result in losses and credit contraction if some of the bleaker outlooks for AI disruption are realized. Some unusual transactions and markdowns related to private credit funds or Business Development Companies run by Blue Owl, Goldman Sachs, and Apollo further unsettled investors.

Middlefield Short Duration Bond Plus launched at the start of February and quickly began building yield while maintaining a low risk profile in this tight credit spread environment. Having approximately a 25% allocation to 2-year Government of Canada bonds has largely provided an offset to any general credit market weakness. The Fund has been measured and selective in adding credit exposure, with well under a year of credit duration. While market volatility in February and into early March created some opportunities to add credit, the magnitude of spread widening was modest relative to already tight starting levels. As a result, the portfolio remains conservatively positioned. The Fund continues to focus on securities that could benefit from embedded options, like being called early at a premium to current pricing or extending past call dates at above market coupons.

Real Estate

Middlefield Fund Tickers & Codes: MREL / MID 600 / RS / RS.PR.A

by Dean Orrico, President & CEO

Amid AI volatility that impacted most sectors of the market, real estate showed resilience with the Canadian REIT index finishing the month up 0.5% and our real estate funds outperforming with a 1.6% return, underscoring the benefits of active management in a dynamic market. Year-to-date, our real estate funds are up 4.3%, outperforming the Canadian REIT index by 0.7% and we continue to see significant runway for further outperformance as fundamentals remain supportive and valuations compelling.

Within our strategies, seniors housing continues to outperform, supported by structurally tight supply, improving operating leverage, and durable demand as the “silver economy” accelerates. We’ve maintained our overweight exposure to seniors housing through Welltower, Extendicare, Sienna and Chartwell, all of which are translating occupancy gains into meaningful NOI growth and margin expansion. In addition, we maintain exposure to the expanding AI theme through our holding in Equinix, a leading global data center REIT that provides the critical infrastructure and interconnection capacity required to support accelerating AI and cloud workloads. With a YTD return of 27.8% as at the end of February, this position has been a meaningful contributor to performance as investor demand for AI-linked infrastructure has strengthened, and the company’s solid 4Q25 results, highlighted by robust bookings and improving growth visibility, further reinforce our conviction in the long-term opportunity.

We’ve been very cautious on the Canadian office market for several years even though we’ve started to see signs of life in major centres like Toronto i.e. Class A properties with attractive amenities are in very short supply/high demand while many Class B/C properties have very high vacancy and have become virtually obsolete. Even though Allied Properties is benefiting from more demand, it has suffered from too much debt and various problematic development projects in Toronto and Vancouver. In an effort to help right-size their balance sheet, they completed a highly dilutive $560 million equity offering in February 2026. While we spent significant time with company management and investment dealers reviewing the opportunity, we concluded that the $10 offering price wasn’t attractive and did not participate. Moreover, as a result of our concerns, we did not own any Allied units and were able to avoid the drawdown from $14 (which was the trading price on February 9 just prior to the announced equity financing).

We continue to have high conviction on Colliers, a global real estate services and investment management platform with diversified operations across brokerage, engineering, and asset management. We’ve seen recent weakness in the name based on fears that AI could automate elements of brokerage and advisory work. We believe these concerns are overstated, as complex leasing transactions and large capital markets mandates remain highly relationship-driven businesses where Colliers’ superior management, scale, and integrated service offering provide a durable competitive advantage.

Healthcare

Middlefield Fund Tickers & Codes: MHCD / MID 325 / SIH.UN

by Dean Orrico, President & CEO

Healthcare benefited from broader market rotation with the S&P 500 Healthcare sector generating a total return of +3.5% during February. Beneath the surface, performance has bifurcated meaningfully, as Biopharma has outperformed on the back of resilient earnings, improving sentiment around pipeline productivity, and investor rotation back into more defensive growth pockets of the market while Life Science Tools & Services have come under pressure amid renewed concerns around AI-driven disruption.

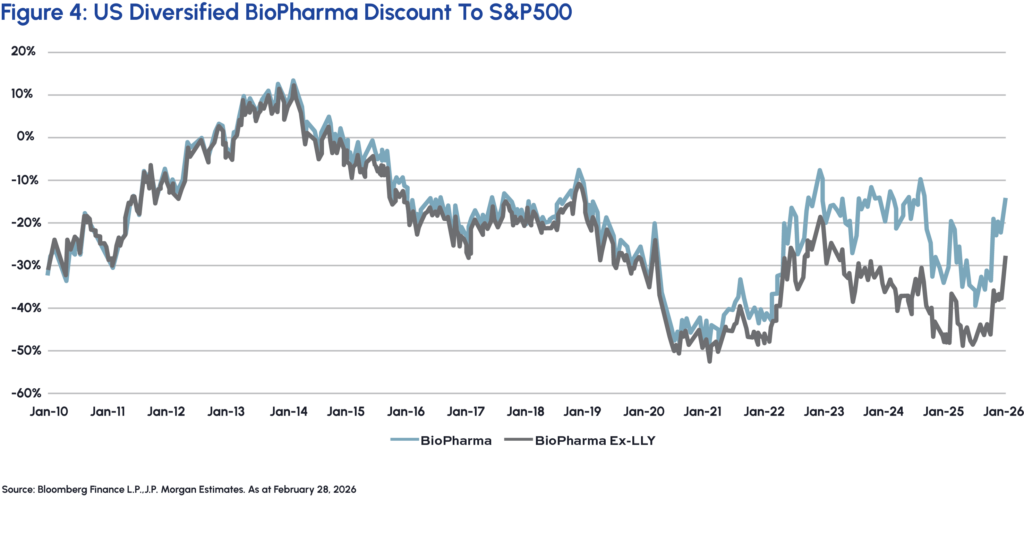

This divergence underscores that healthcare is far from a concentrated “three stock strategy,” as evidenced by double-digit drawdowns this year in widely held names such as UnitedHealth (-14%) and Novo Nordisk (-25%). In this environment active positioning has been critical with drug distributors emerging as an area of relative strength where we remain overweight through names such as McKesson and Cardinal Health. Despite a six-month rally from September lows, diversified biopharma continues to trade at a meaningful discount to the S&P 500, which we continue to view as an attractive entry point. We remain constructive given the FDA’s formalization of a “One Pivotal Trial” pathway, under which a single well-controlled study may be sufficient for approval in certain cases. While the agency retains flexibility to require multiple trials when uncertainty is higher, a clearer one-trial framework should lower development costs, shorten timelines, and potentially increase the number of assets advancing into the clinic. Over time, we see this as supportive of innovation, capital efficiency, and earnings durability across high-quality biopharma franchises.

We recently attended TD Cowen’s Healthcare Conference in Boston which brought together industry leaders to discuss the evolving landscape of pharmaceuticals, biotechnology, and MedTech. A prominent narrative throughout the conference centered on the accelerating integration of AI, and its rapidly expanding role across the entire drug development process. Companies are seeing AI as a powerful tool to significantly speed up R&D timelines, with some noting a 30% reduction in the time it takes to get a new molecule from discovery to initial human trials, shortening a typical three-year process to two. This is achieved by AI helping chemists design and refine compounds more efficiently, leading to higher quality potential medicines and fewer wasted efforts. Furthermore, AI is showing promise in connecting patients to clinical trials more effectively and ensuring that approved drugs reach the right patients more quickly, tackling issues like diagnosis delays and access. This shift will become a fundamental change in how the industry operates, driven by the need to be more efficient, reduce costs, and accelerate the delivery of life-changing treatments to patients.

We recently attended TD Cowen’s Healthcare Conference in Boston which brought together industry leaders to discuss the evolving landscape of pharmaceuticals, biotechnology, and MedTech. A prominent narrative throughout the conference centered on the accelerating integration of AI, and its rapidly expanding role across the entire drug development process. Companies are seeing AI as a powerful tool to significantly speed up R&D timelines, with some noting a 30% reduction in the time it takes to get a new molecule from discovery to initial human trials, shortening a typical three-year process to two. This is achieved by AI helping chemists design and refine compounds more efficiently, leading to higher quality potential medicines and fewer wasted efforts. Furthermore, AI is showing promise in connecting patients to clinical trials more effectively and ensuring that approved drugs reach the right patients more quickly, tackling issues like diagnosis delays and access. This shift will become a fundamental change in how the industry operates, driven by the need to be more efficient, reduce costs, and accelerate the delivery of life-changing treatments to patients.

Infrastructure

Middlefield Fund Tickers & Codes: MINF / MID 265 / MID 510 / ENS / IS / IS.PR.A

Energy and Utilities were among the strongest performing sectors over the past month and year-to-date across both the S&P 500 and S&P/TSX Composite Indices, as volatility and geopolitical uncertainty reinforced the market’s preference for resilient, cash flow–oriented businesses. Higher crude prices and sustained capital discipline have supported free cash flow durability across energy, while regulated utilities and pipeline operators have outperformed on the strength of contracted revenue models, solid balance sheets, and limited exposure to technological disruption risk. Both TC Energy and Enbridge delivered strong fourth-quarter results. TC Energy exceeded expectations, raised its dividend by 3%, (26th consecutive annual increase), and reaffirmed 5–7% adjusted EBITDA growth through 2028, supporting targeted dividend growth of 3–5%. Management also highlighted approximately $8 billion of high-probability projects expected to be sanctioned in 2026, reinforcing visible medium-term growth. Enbridge also demonstrated a clear path to ~5% annual growth through the end of the decade. The company reiterated its 2026 outlook while advancing incremental projects, underscoring balance sheet strength and cash flow stability. We continue to view both companies as core long-term holdings across our funds.

A recent management meeting resulted in an increasingly constructive stance on Brookfield Renewable Partners (BEP) due to the nuclear opportunity within its ownership in Westinghouse. Nuclear projects advancing in the U.S. and renewed multi-billion-dollar commitments from Japan to invest in U.S. power and energy infrastructure meaningfully enhances its long-duration growth profile. Concurrently, BEP’s Solar and Battery segments are delivering some of the highest growth rates within the portfolio, supported by durable tailwinds including AI-driven data centre demand, industrialization, and electrification. A constructive capital recycling environment coupled with differentiated origination capabilities through Brookfield Asset Management (further aligned with Connor Teskey serving as CEO of both entities), supports disciplined acquisitions at attractive returns.

TransAlta continues to advance its Alberta data centre strategy announcing a MOU with Brookfield and CPP Investments, positioning the company to benefit from rising utilization as a phased buildout plan progresses. We continue to favour utility and power names across our portfolios given their alignment with structural demand trends and proactive approach to secure contracts with hyperscalers.

Technology & Communications

Middlefield Fund Tickers & Codes: MINN / SIH.UN / MID 925 / MDIV

by Shane Obata, Portfolio Manager

Despite recent bouts of market volatility, the Technology sector continues to decouple from the broader market in the metric that matters most: earnings power. While the S&P 500 is projected to deliver a respectable 14% EPS growth in 2026, the indication from Technology is significantly stronger. Current consensus estimates suggest the sector will deliver the market’s best performance with approximately 33% year-over-year EPS growth. It is crucial to understand that this divergence is not driven by speculative valuation expansion; rather, it is the result of fundamental operating leverage derived from the most significant capital expenditure cycle in industrial history.

As the AI cycle accelerates, our excitement is shifting from the sheer scale of the spend to the broadening of its beneficiaries. While recent results from industry titans like NVIDIA and Broadcom confirm our hypothesis that the infrastructure buildout is more durable than consensus expected, the most notable development is how positive earnings revisions are cascading into the broader supply chain. We are seeing a powerful “HALO effect” lift adjacent industries, specifically memory & storage and semiconductor capital equipment.

Furthermore, while raw compute capacity remains the primary bottleneck for AI scaling, the infrastructure required to connect these massive clusters is becoming equally critical. As data centers expand to gigawatt levels, the ability to move vast amounts of data between GPUs with minimal latency is paramount to unlocking their full potential. This dynamic is driving an explosive upgrade cycle in advanced networking and optics, creating a new class of winners essential to the “nervous system” of AI clusters.

Finally, regarding the Software industry, we remain disciplined despite the recent market scrutiny. We do not believe software is “doomed,” and the existential risks regarding AI disruption and the erosion of seat-based pricing models remain unresolved. As AI agents increasingly automate workflows, the deflationary pressure on legacy SaaS revenue models suggests that terminal valuation multiples should permanently re-rate lower to reflect higher long-term risk. Rather than attempting to time a bottom in software or guess which incumbents will successfully navigate this pivot, we are using market weakness to add to the companies profiting today.

Resources

Middlefield Fund Tickers & Codes: MID 800 / MID 161 / MID 265 / MRF FT LP / Discovery FT LP

by Dennis da Silva, Senior Portfolio Manager

Gold and gold equities significantly outperformed broad North American markets in February with bullion and the S&P/TSX Gold Index up 8.5% and 23.6% respectively versus a negative 0.7% return for the S&P 500. Gold equities look to be breaking out of a sideways channel versus the S&P 500 as seen in the below graph. Traditional factors driving gold higher remain firmly in place, but we also note some key differences vs prior cycles that could extend its longevity, including central banks being major net buyers, erosion in international confidence and elevated global sovereign debt burdens. Since the 2022 cycle low, gold has appreciated an impressive 220% however history points to material upside. If the current cycle were to replicate previous bull cycles such as 1976-1980, 2001-2008 or 2001–2011, the implied price 2-3 years forward would extrapolate to between US$8,000-US$10,000/ an ounce. Despite ongoing producer discipline, strong balance sheets, record margins and free cashflow generalist investors remain underweight the gold equity sector. Capital allocation is beginning to reflect the shift in gold miners’ fortunes. Buybacks, dividend increases, and special dividends are recurring themes so far this year, signaling growing confidence in balance sheets and sustainability of cash flows. Will substantial M&A be next?

The energy markets in February and early March have endured a dramatic shift from a “supply surplus” to an acute “geopolitical crisis” narrative. The S&P/TSX Capped Energy Index was up 10.6% in February, with a modest gain of 2.8% for oil despite the 34.3% correction in spot natural gas after a rapid rise during the January cold snap. While the first half of the month saw oil prices suppressed by high U.S. oil inventory builds and warming weather trends, a major escalation in the Middle East into month end sent shockwaves through global energy markets. Early in March, operation Epic Fury has accelerated global energy commodity prices and related equity prices higher given roughly 20% of the world’s crude oil and LNG is being restricted through the Strait of Hormuz. If the closure of the Strait of Hormuz extends beyond the next couple of weeks oil prices may sustain north of US$100/bbl throughout Q1 and into Q2. European natural gas prices have nearly doubled since mid-February due to the sudden disruption of LNG shipments at a time where natural gas storage levels are approximately 50% lower than the same period in 2025 and 2024. History suggests energy prices will fade as soon as supply is restored, however it is likely that current events will drive a structurally higher risk premium for prices.

Exchange Traded Funds (ETFs)

Mutual Funds (FE | F)

TSX-Listed Closed-End Funds

| Fund | Ticker | Strategy |

|---|---|---|

| MINT Income Fund | MID.UN | Equity Income |

| Sustainable Innovation & Health Dividend Fund | SIH.UN | Innovation & Healthcare |

TSX-Listed Split Share Corps. (Class A | Preferred)

| Fund | Ticker | Strategy |

|---|---|---|

| E-Split Corp. | ENS | ENS.PR.A | Energy Infrastructure |

| Real Estate Split Corp. | RS | RS.PR.A | Real Estate |

| Infrastructure Dividend Split Corp. | IS | IS.PR.A | Infrastructure |

LSE-Listed Fund

| Fund | Ticker | Strategy |

|---|---|---|

| Middlefield Canadian Enhanced Income UCITS ETF | LSE: MCTC | LSE: MCTP | Canadian Equity Income |

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments, including ETFs. Please read the prospectus before investing. You will usually pay brokerage fees to your dealer if you purchase or sell units/shares of investment funds on the Toronto Stock Exchange or other alternative Canadian trading system (an “Exchange”). If the units/shares are purchased or sold on an Exchange, investors may pay more than the current net asset value when buying and may receive less than the current net asset value when selling them. There are ongoing fees and expenses associated with owning units or shares of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in these documents. Mutual funds and investment funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain statements in this disclosure are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may”, “will”, “should”, “could”, “expect”, “anticipate”, “intend”, “plan”, “believe”, or “estimate”, or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what Middlefield Funds and the portfolio manager believe to be reasonable assumptions, neither Middlefield Funds nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

This material has been prepared for informational purposes only without regard to any particular user’s investment objectives or financial situation. This communication constitutes neither a recommendation to enter into a particular transaction nor a representation that any product described herein is suitable or appropriate for you. Investment decisions should be made with guidance from a qualified professional. The opinions contained in this report are solely those of Middlefield Limited (“ML”) and are subject to change without notice. ML makes every effort to ensure that the information has been derived from sources believed to reliable, but we cannot represent that they are complete or accurate. However, ML assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. ML is under no obligation to update the information contained herein. This document is not to be construed as a solicitation, recommendation or offer to buy or sell any security, financial product or instrument.