Index

Launch of Fixed Income Strategy

Since December of last year, the Bank of Canada overnight lending rate dropped from 3.75% to 2.25%. At the same time, the Federal Reserve has reduced the lower bound of its target rate from 4.5% to 3.75%, with 3 more 25 basis point cuts expected through 2026. These central bank interest rate cuts have led to a reduction in cash yields. Indicated net yields on the largest high interest saving funds in Canada have fallen to the low 2% area. Investors focused on the preservation of capital are being pressured to accept much lower returns with central banks in an easing cycle. Middlefield has created a solution for advisors and in the new year is excited to launch a flexible, multi-sector, short-duration fixed income strategy that will aim to enhance the returns available to low-risk investors while maintaining a focus on liquidity and capital preservation. Middlefield intends to offer the Short Duration Bond Plus Fund in both a mutual fund and ETF format.

Macro Update

by Dean Orrico, President & CEO and Robert Lauzon, Managing Director & CIO

Equity markets have been choppy recently with the U.S. government shutdown and AI bubble concerns contributing to a pattern of sharp market fluctuations. Despite the turbulence, the S&P 500 managed to eke out a seventh consecutive month of positive returns (+0.2%) thanks to a 3.7% rebound during the final week of trading. The TSX followed a similar path directionally but delivered a better result with a total monthly return of 3.7%.

Despite the S&P 500 being flat in November, a significant market rotation took place under the surface. Information Technology (-4.3%), Consumer Discretionary (-2.4%) and Industrials (-0.9%) lagged while the other eight sectors in the Index generated returns ranging from +1.8% to +9.3%. This pattern is consistent with the market broadening theme we have been anticipating for several months and is a trend we expect to continue in 2026. With relative valuations for most sectors remaining cheap (highlighted below in blue), we see additional upside available in several of our core sectors including Healthcare, Real Estate, Financials and Energy.

We have held a constructive view on Canadian equities throughout 2025. Our thesis has been grounded in a clear shift in policy direction, with multiple levels of government prioritizing long-duration infrastructure and economic growth initiatives. Recent developments, including the Alberta–Canada MOU and the Federal Budget, provide tangible evidence that the capital investment cycle is accelerating. Major projects such as the West Coast pipeline expansion, the Pathways Alliance carbon capture initiative, large-scale data centre buildouts, and continued additions to Canada’s energy and power capacity collectively point to a multi-year tailwind for the domestic economy. With Canadian equities expected to deliver earnings growth comparable to the U.S. while trading at a roughly 6x P/E discount, we see a compelling case for continued relative outperformance. We remain bullish on Canadian companies exposed to this buildout, particularly in energy and energy infrastructure, industrials, real estate, and financials, all of which stand to benefit from rising capital investments tied to this national investment agenda.

The longest U.S. government shutdown in history officially ended on November 12 after 43 days. While markets seemed relatively unfazed in the immediate term, the shutdown is likely to have ripple effects. For example, the cancellation of key economic releases including the October jobs report, CPI data and monthly retail sales leaves the Federal Reserve without key data points ahead of its December meeting. Despite the imperfect information, futures markets are pricing in a 95% probability of a rate cut on December 10 at the Fed’s final meeting of the year. We agree the Fed is likely to cut and expect another 2–3 rate cuts in 2026 as inflation gradually comes down and the job market normalizes after an extended period of tightness. Insofar as employment dynamics are normalizing, and don’t deteriorate, we think Fed cuts will be received positively by the market next year and support increased business activity throughout the economy.

Real Estate

Middlefield Fund Tickers & Codes: MREL / MID 600 / RS / RS.PR.A

by Dean Orrico, President & CEO

The Canadian REIT sector experienced a modest pullback this month, with the TSX Capped REIT Index declining 0.6%. Notwithstanding this pause, MREL and MID 600 both pulled ahead of the Canadian REIT benchmark for the year with total returns of approximately 11% to the end of November. Our conviction in the sector remains unchanged as underlying fundamentals across retail, industrial, multi-family and seniors housing continue to strengthen, supported by declining interest rates, healthy private-market demand, and improving capital flows into the sector. We believe these dynamics position REITs for renewed momentum, with meaningful upside potential as we move into 2026.

We attended RioCan’s investor day this month and subsequently met with management in our offices. Their 2026–2028 outlook calls for core FFO growth of at least 3.5% underpinned by a combination of same-property NOI growth and capital recycling. Long-term, RioCan expects to deliver at least 5% annual earnings growth, supported by a mark-to-market rent opportunity exceeding 25%. Jonathan Gitlin, RioCan’s CEO, stated he has never had more conviction in the portfolio’s fundamentals, citing Canada’s improving economic backdrop, high barriers to new urban retail supply, and an increasingly diverse tenant base looking to expand brick-and-mortar footprints. RioCan enters the next phase of its strategy with a high concentration in the country’s largest metropolitan areas and its planned portfolio repositioning mostly complete, resulting in enhanced visibility and a more resilient earnings profile.

Given our positive outlook and intimate knowledge of the seniors housing sector, we were early in building a position in Extendicare (EXE) several years ago. Since then, the market has adopted our view that both its long-term care (LTC) and home healthcare businesses were poised for significant growth potential. That view has been reflected in EXE’s share price which has climbed from the mid-single digits to over $20 in the past 18 months. We continue to see further upside, driven primarily by the accelerating growth of its home healthcare platform, which delivered 13% year-over-year organic growth in Q3. Organic gains are also being amplified by several acquisitions, including the recently announced transformative $570 million purchase of CBI Home Health – a deal that will nearly double the size of EXE’s home care operations. CBI is a national home health care company that will diversify and expand EXE’s geographic footprint with a notable presence in Alberta. EXE’s rapidly expanding home health care segment is complemented by its stable, steadily improving LTC business, which has returned to its pre-COVID predictability and is benefiting from favourable government funding tailwinds. This foundation provides predictable cash flows and clear visibility into future growth, reinforcing our conviction in the company’s long-term outlook.

Healthcare

Middlefield Fund Tickers & Codes: MHCD / MID 325 / SIH.UN

by Robert Moffat, Portfolio Manager

Healthcare had an exceptional month of November, generating a total return of 9.3%. The sector has been a beneficiary of market rotation dynamics amidst recent volatility in the AI landscape. Looking ahead, we remain very constructive on healthcare and believe the recent streak of outperformance can continue in 2026. This view is underpinned by an improving policy outlook, increased M&A activity, clinical catalysts and earnings growth from new product launches.

Pharma was the top-performing sub-industry this month, generating a total return of 16.4%. Drug pricing developments have been the biggest catalyst for the sector with five most-favoured nation (MFN) related agreements now in place. While each deal carries its own nuances, they collectively demonstrate that MFN risks are being contained and shaped by company-specific considerations. Through this lens, the recent agreement between the White House and Eli Lilly / Novo Nordisk was particularly important. It introduced meaningful pricing clarity in GLP-1s, while also signaling explicit government support for obesity medications through expanded access in the Medicare channel. As we noted after Pfizer’s MFN deal in late September, the sector’s valuation discount had plenty of room to narrow if sentiment continued to improve, and that dynamic is playing out. Even after the recent rally, pharma still trades at a notable 5x P/E discount to the broader market, suggesting more upside toward its historical median P/E spread of ~2x.

The M&A wave across healthcare continued this month, featuring notable transactions from two of our portfolio companies. Abbott announced the acquisition of Exact Sciences for $21 billion, a strategic move that bolsters its diagnostics platform and expands its presence in high-growth cancer screening. Merck announced a $9.2 billion acquisition of Cidara Therapeutics, driven by interest in its long-acting antiviral aimed at universal influenza prevention. A key tenet of our investment thesis in each company is their strong balance sheets and ability to deploy capital into strategic business development opportunities that strengthen long-term growth. Both companies have demonstrated a consistent track record of disciplined M&A execution and integration in the past and we view these latest deals as strategically sound and supportive of future value creation.

Infrastructure

Middlefield Fund Tickers & Codes: MINF / MID 265 / MID 510 / ENS / IS / IS.PR.A

by Robert Lauzon, Managing Director & CIO

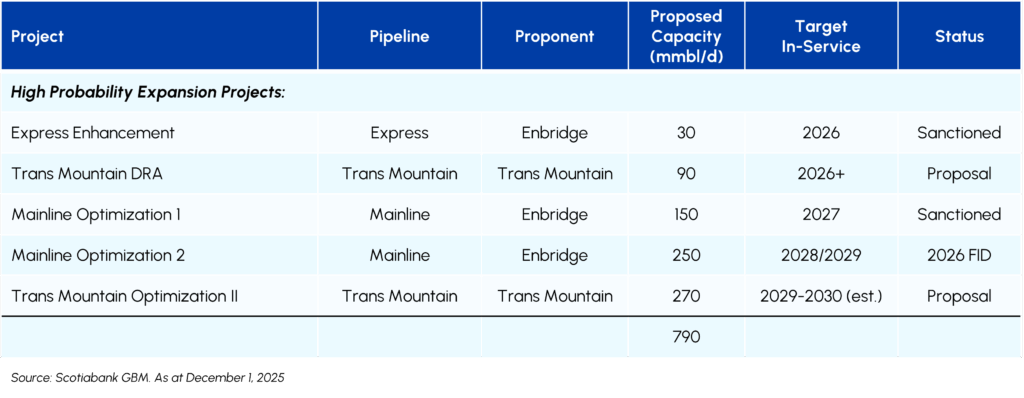

Canada’s energy infrastructure backdrop continues to strengthen as policy alignment between federal and provincial governments accelerates the approval and execution of nationally significant projects. The recent MOU between Canada and Alberta marks the clearest shift in more than a decade toward coordinated energy development, materially reducing uncertainty around accelerated timelines for carbon capture hubs, LNG expansion, new pipelines, rail connectivity, and large-scale electricity transmission. This shift positions Canada to enhance export capacity and global competitiveness, with ~800 mmbl/d of additional pipeline capacity and optimizations potentially available before the end of the decade. The momentum is equally strong across the broader ecosystem: producers benefit from clearer emissions frameworks and improved egress visibility; pipelines see renewed potential for long-duration, contracted growth; and utilities stand to deploy meaningful capital into flexible generation as demand rises from electrification, AI data centers, and industrial load.

AltaGas, Gibson Energy, and Enbridge have reinforced this constructive backdrop with guidance pointing to steady mid-single-digit EBITDA growth and disciplined capital investment. Across these companies, several billion dollars of projects are expected to come online through the end of the decade, supporting consistent dividend growth and extending visibility into long-term cash flow growth. As multi-year investment cycles take shape, the overall sector momentum remains constructive and supports our positioning across core Canadian infrastructure themes. Our core holdings include Tourmaline, Enbridge, and AltaGas, which are all well placed to benefit from further development, higher throughput, and growing long-duration infrastructure needs.

In parallel, global infrastructure spending is accelerating, and Brookfield has emerged as one of the most influential participants in this new investment cycle. Recent announcements, including Brookfield’s role in an $80B U.S. nuclear deployment program (through Westinghouse) and the launch of a $100B AI infrastructure fund with NVIDIA and the Kuwait Investment Authority, underscores the scale of capital now mobilizing to address structural power shortages and the rapid growth of digital load. These initiatives will help bridge the gap between intermittent renewables and the firm, long-duration capacity required for industrial demand and AI compute, while reinforcing the value of diversified, large-scale platforms capable of delivering generation, transmission, storage, and data-center infrastructure. Through Brookfield Renewable Partners, our portfolios maintain direct exposure to these long-term themes, complementing our Canadian infrastructure holdings and enhancing our overall positioning toward the energy transformation and AI-driven power-demand cycle.

Technology & Communications

Middlefield Fund Tickers & Codes: MINN / SIH.UN / MID 925 / MDIV

by Shane Obata, Portfolio Manager

While the Technology sector is set to deliver approximately 25% EPS growth in aggregate for 2026, we anticipate a sharp bifurcation between AI “winners” and “losers” as the market moves past the initial hype phase. Our active investment strategy is positioned for this shift by capitalizing on high-conviction ideas outside the crowded Magnificent Seven trade, particularly in international markets where valuations remain attractive relative to growth potential.

The next phase of the AI trade will not be defined by who can build the largest infrastructure, but by who can deploy it to create indispensable value. While AI models continue to impress on standardized tests, 2026 must be the year where technical benchmarks take a backseat to real-world utility. To date, much of the excitement has been theoretical, but for cloud giants to justify their massive capital outlays, the end-users—both enterprises and consumers—must see a tangible return on investment. We expect “Agentic AI” to play a central role in this narrative, where software doesn’t just summarize text but autonomously executes multi-step business processes. This transition is critical as consumers and businesses need to derive enough value to pay for these services, which is the only way the cloud companies will generate acceptable returns on their own record-breaking investments.

Within this evolving landscape, market sentiment has arguably swung too aggressively in favor of the “Google complex” following recent Gemini momentum, potentially discounting the entrenched nature of the “OpenAI complex.” While competitors have closed the technical gap, OpenAI remains the clear leader in adoption, boasting engagement levels that dwarf the competition. We believe the market’s concerns regarding their financial viability are a solvable monetization issue rather than a fatal structural flaw. We expect OpenAI to shortly release a new competitive model that re-establishes its technical prowess and alleviates fears about its staying power. Furthermore, the company must accelerate plans to monetize its vast non-subscriber base, likely through an ad-supported tier. This transition from a pure subscription model to a hybrid revenue stream is the key to stabilizing its cash burn and proving that the current leader in adoption can also become a leader in sustainable profitability.

Resources

Middlefield Fund Tickers & Codes: MID 800 / MID 161 / MID 265 / MRF FT LP / Discovery FT LP

by Dennis da Silva, Senior Portfolio Manager

After a volatile month in October, gold settled into a trading range between US$4,000 and $4,200/oz during November. Gold equities significantly outperformed the commodity with the S&P/TSX Gold Index returning 16%. While central banks and investors remain key pillars of gold demand, Tether has emerged as a meaningful new buyer, acquiring 26 tonnes in Q3 2025 and outpacing every central bank’s purchase during the quarter. Recent data shows how Tether is increasingly gaining influence on the gold market through physical gold purchases, holding around 116 tons of gold with a value of approximately US$14 billion. At the center of Tether’s strategy is “tokenized gold”, specifically the Token Tether Gold. This is a digital representation of physical gold that is mapped on the blockchain and is intended to grant the owner direct claim to deposited bars. Tether is also investing in companies that are directly linked to the cash flows of gold mines through gold royalties and streaming models, having invested around US$300 million in four companies.

We continue to see a positive backdrop for natural gas producers. Natural gas prices rose 17.6% during the month, mostly supported by colder weather. The longer-term outlook is structurally positive as well, anchored by rising LNG export capacity and accelerating demand from AI-driven data centres. LNG Canada’s ramp-up should meaningfully shift the supply-demand balance for Western Canadian producers, similar to the step-change seen in heavy crude markets after Trans Mountain came online. Canadian energy producers have resilient cash flows from lower decline rates and deeper drilling inventories relative to U.S. peers, making then an attractive way to gain exposure to the natural gas theme.

Exchange Traded Funds (ETFs)

Mutual Funds (FE | F)

TSX-Listed Closed-End Funds

| Fund | Ticker | Strategy |

|---|---|---|

| MINT Income Fund | MID.UN | Equity Income |

| Sustainable Innovation & Health Dividend Fund | SIH.UN | Innovation & Healthcare |

TSX-Listed Split Share Corps. (Class A | Preferred)

| Fund | Ticker | Strategy |

|---|---|---|

| E-Split Corp. | ENS | ENS.PR.A | Energy Infrastructure |

| Real Estate Split Corp. | RS | RS.PR.A | Real Estate |

| Infrastructure Dividend Split Corp. | IS | IS.PR.A | Infrastructure |

LSE-Listed Fund

| Fund | Ticker | Strategy |

|---|---|---|

| Middlefield Canadian Enhanced Income UCITS ETF | LSE: MCTC | LSE: MCTP | Canadian Equity Income |

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments, including ETFs. Please read the prospectus before investing. You will usually pay brokerage fees to your dealer if you purchase or sell units/shares of investment funds on the Toronto Stock Exchange or other alternative Canadian trading system (an “Exchange”). If the units/shares are purchased or sold on an Exchange, investors may pay more than the current net asset value when buying and may receive less than the current net asset value when selling them. There are ongoing fees and expenses associated with owning units or shares of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in these documents. Mutual funds and investment funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain statements in this disclosure are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may”, “will”, “should”, “could”, “expect”, “anticipate”, “intend”, “plan”, “believe”, or “estimate”, or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what Middlefield Funds and the portfolio manager believe to be reasonable assumptions, neither Middlefield Funds nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

This material has been prepared for informational purposes only without regard to any particular user’s investment objectives or financial situation. This communication constitutes neither a recommendation to enter into a particular transaction nor a representation that any product described herein is suitable or appropriate for you. Investment decisions should be made with guidance from a qualified professional. The opinions contained in this report are solely those of Middlefield Limited (“ML”) and are subject to change without notice. ML makes every effort to ensure that the information has been derived from sources believed to reliable, but we cannot represent that they are complete or accurate. However, ML assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. ML is under no obligation to update the information contained herein. This document is not to be construed as a solicitation, recommendation or offer to buy or sell any security, financial product or instrument.